Trade Friction Reshapes Global MEG Trade Flow

By:

- Alan Lu, Director, China Aromatics & Fibres, Chemical Market Analytics by OPIS

In 2025, mainland China’s monoethylene glycol (MEG) consumption is projected to reach 28.18 million metric tons (mt), accounting for approximately 68% of total global demand. Despite the launch of numerous domestic conventional and coal-to-MEG (CTM) projects in recent years, which have significantly enhanced domestic MEG supply, the mainland Chinese MEG market continues to face a notable supply deficit.

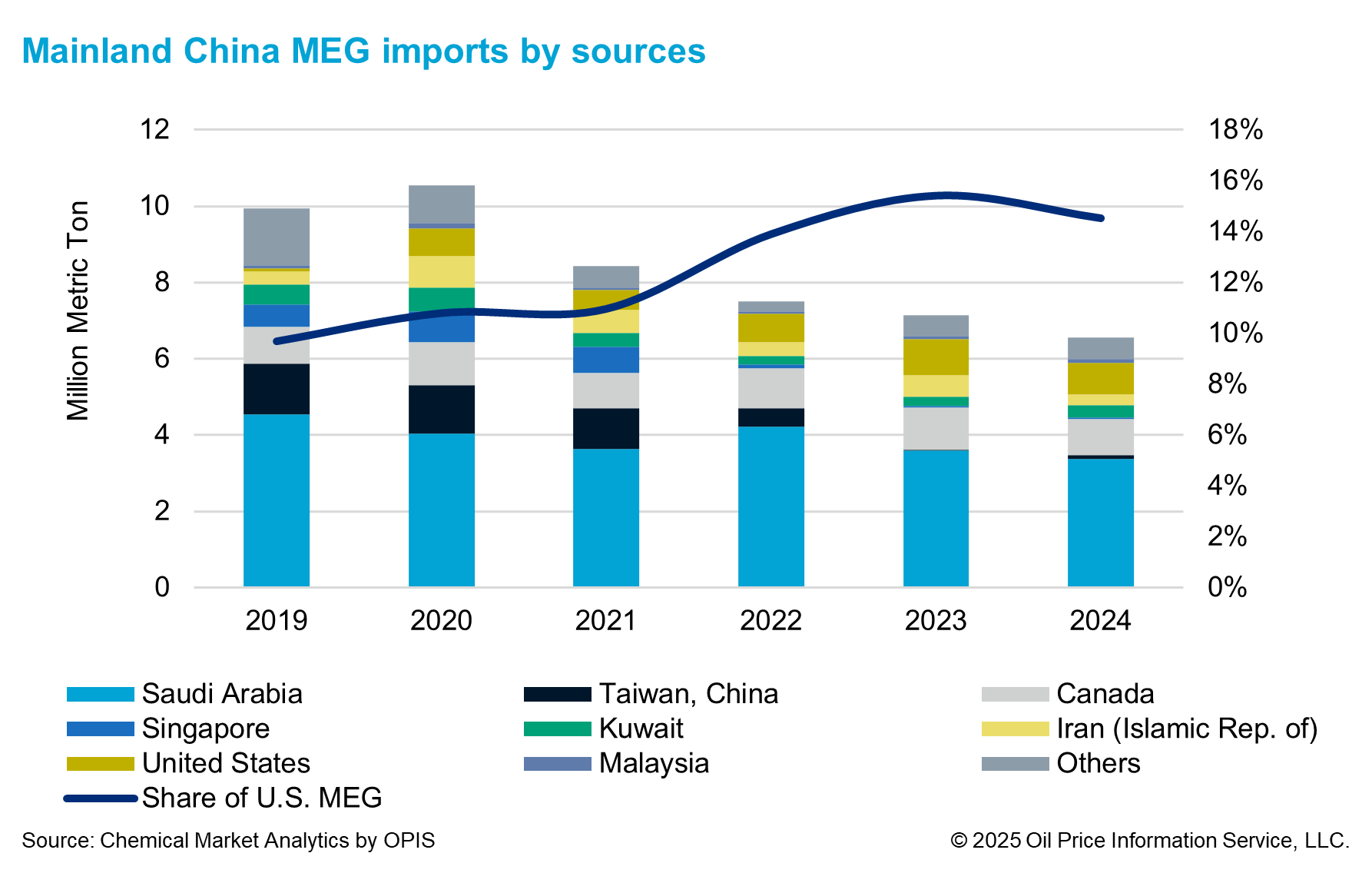

This shortfall is driven by sustained, robust growth in the downstream polyester market, necessitating a reliance on imports. The United States ranked as the third-largest import source, supplying 12.5% of mainland China’s total MEG imports in 2024, trailing only Saudi Arabia and Canada.

In 2025, mainland China’s monoethylene glycol (MEG) consumption is projected to reach 28.18 million metric tons (mt), accounting for approximately 68% of total global demand

The U.S.-China trade relationship experienced an escalation of tensions following the “Liberation Day tariffs” on April 2, 2025, a situation that persisted until May 11, 2025. On that date, both countries agreed to reduce their average reciprocal tariff rates to 10%, a measure that excluded the 20% U.S. tariff on fentanyl from mainland China and any tariffs already in place before the “Liberation Day tariffs.”

Given that MEG is a key globally traded petrochemical product with a significant impact on the balance of both the U.S. and mainland Chinese markets, this report provides an analysis of how ongoing U.S.-China trade friction is affecting the international MEG trade landscape.

As of September 1, 2025, mainland Chinese companies importing U.S.-origin MEG are subject to three types of tariffs:

- – 5.5% base tariff;

- – 10% reciprocal tariff;

- – 25% retaliatory tariff originally imposed in 2019 (companies can apply to customs for an exemption).

Before the “Liberation Day tariffs,” the vast majority of mainland Chinese importers of U.S.-origin MEG successfully obtained the 25% tariff exemption, effectively paying only the 5.5% base tariff. After this event, however, even with the high-tariff exemption, importers must still bear the 10% reciprocal tariff.

This rate is significantly higher than the actual market price difference between U.S.-origin MEG and that from other countries, rendering U.S.-origin MEG almost uncompetitive in the mainland Chinese market under normal trade conditions.

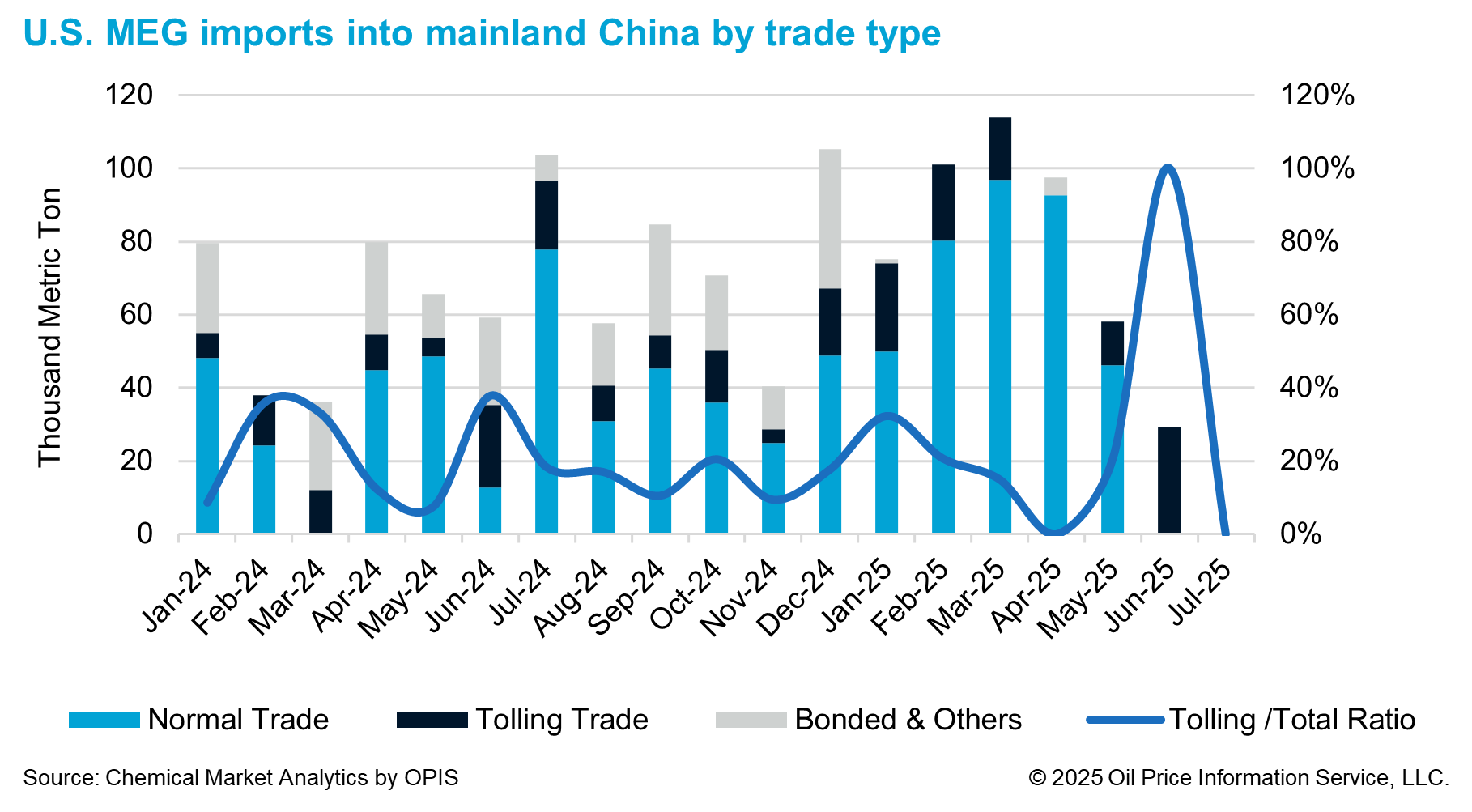

As illustrated in Figure 2, from January to December 2024, mainland China’s average monthly MEG import from the U.S. was approximately 68,000 mt. This figure rose to 100,000 mt per month from January to April 2025, but has since shown a precipitous decline starting in May, fully reflecting the impact of the trade friction on U.S.-China MEG trade.

Beyond the normal trade category, mainland China’s MEG imports are also predominantly conducted via tolling trade and bonded trade. Tolling trade is common among companies that export polyester bottle resin or polyester fibers, as this method allows them to import feedstock without paying any tariffs, including the base tariff. Bonded trade, meanwhile, is widely used for future resale as imported cargo or to meet the need for delayed customs declaration.

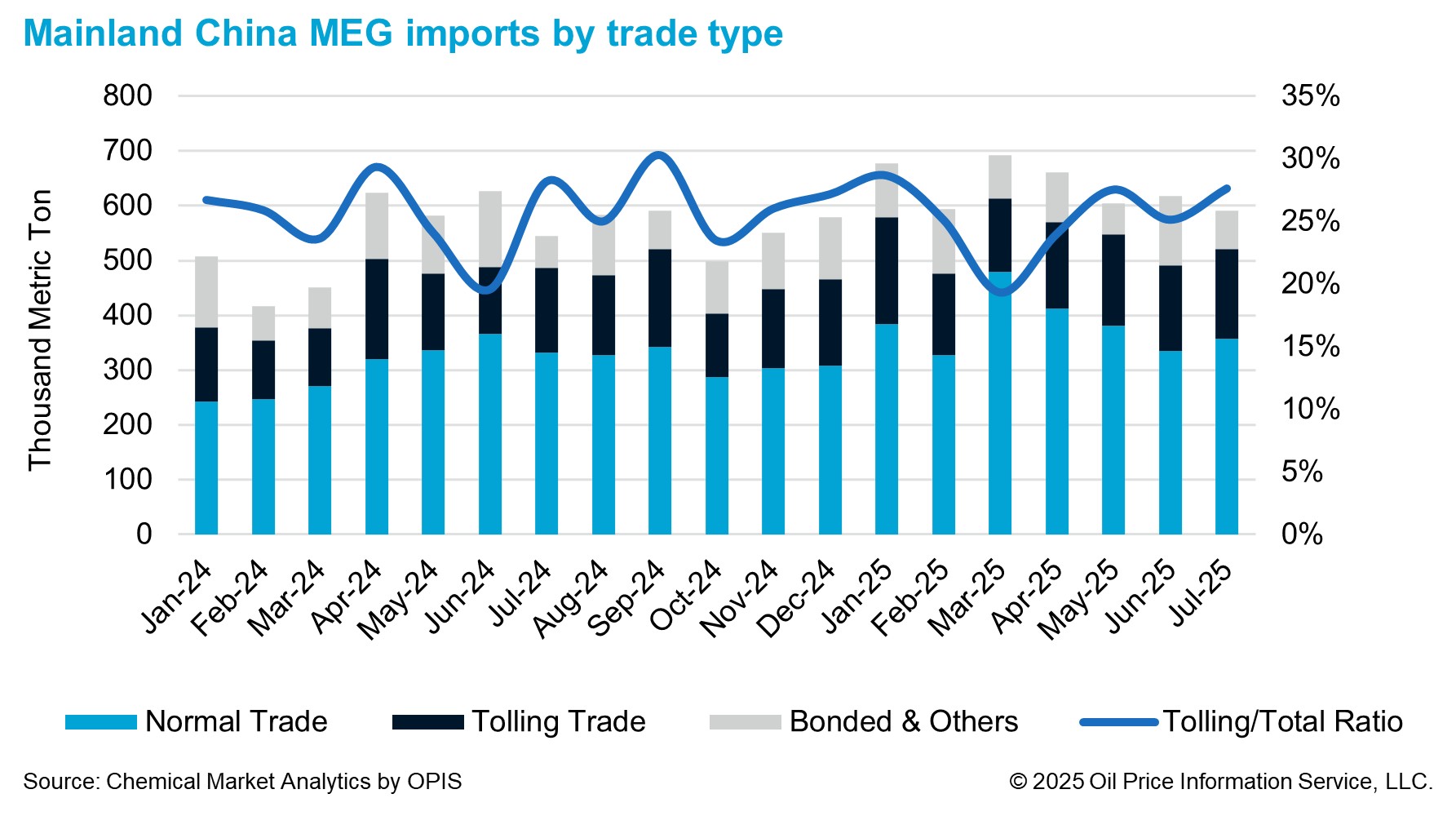

As shown in Figure 3, tolling trade accounts for approximately a quarter of mainland China’s total MEG imports, with its ratio to normal trade consistently maintained at roughly 3:7. With mainland China’s monthly polyester exports exceeding one million mt, there is theoretically a great upside for MEG imports under the tolling trade category.

Notably, from January 2024 to March 2025, about 20% of U.S.-origin MEG were imported into mainland China via tolling trade, but this share saw a significant decline after April 2025 (Figure 2). This trend is primarily due to mainland Chinese polyester producers proactively avoiding U.S.-origin MEG even for tolling trade. They are motivated by concerns over geopolitical and operational uncertainties, even though this trade process is not theoretically constrained by reciprocal tariffs.

However, the total volume of mainland China’s MEG imports under tolling trade did not decrease after April 2025, as supplies from Saudi Arabia, Canada, Kuwait, and other countries quickly filled the void left by the U.S.

From the perspective of U.S. MEG exports, another significant shift is evident. While the post-trade-war recovery in MEG exports from the U.S. can be partially attributed to increased production following the end of a heavy turnaround season, the trade conflict impact on the U.S. MEG exporting structure remains highly apparent.

From January 2024 to March 2025, mainland China’s share of total U.S. MEG exports averaged 29%; however, this proportion plummeted to just 2% from April to July 2025.

For every winner, there’s a loser. The U.S. MEG that is disappearing from the mainland Chinese market is now being redirected to other regions.

Starting in April 2025, U.S. MEG exports to Turkey and India saw a notable increase, with these two countries displacing mainland China as the largest markets for U.S. MEG during this period. When compounded by the observed increase in exports from the Middle East and Canada to mainland China, it becomes clear that a significant swap of trade flows has taken place, gradually reshaping the global MEG trade landscape.

Market Advisory Service: Asia Aromatics

Comprehensive insights across feedstocks and major downstream products

Amid persistent geopolitical uncertainty, the development of the trade conflict and its implications are unrealistic to predict.

Nonetheless, barring a structural change in current tariff policies, Chemical Market Analytics projects that U.S. MEG exports to mainland China will primarily be limited to volumes under long-term contracts.

Any extra spot trade will require a large enough price discount to attract mainland Chinese buyers to take position.

Whether for contract or spot volumes, mainland Chinese companies are expected to primarily import U.S. origin MEG under tolling trade category.

Furthermore, the upside for MEG imports into emerging markets such as Turkey and India to act as substitutes for the mainland Chinese market will also influence the future structure of U.S. MEG exports. In a context of high supply, the U.S. will either need to open up additional alternative markets or be compelled to increase exports to mainland China at more competitive prices.

Both scenarios could further widen the price gap between the U.S. and mainland Chinese markets.