Why Expert PVC Price Analysis and Forecasting Are Critical for Informed Decision-Making

Introduction

This article is the first in a series of informational publications provided without charge by Chemical Market Analytics by OPIS, a Dow Jones company, to interested parties who produce or consume polyvinylchloride (PVC) or who otherwise have interests in the PVC market. For further information, please contact Ana.Lopez@chemicalmarketanalytics.com

PVC pricing and forecasting require integrated analysis of global supply–demand balances, production cost structures, and trade dynamics to support informed sourcing, investment, and planning decisions.

Summary

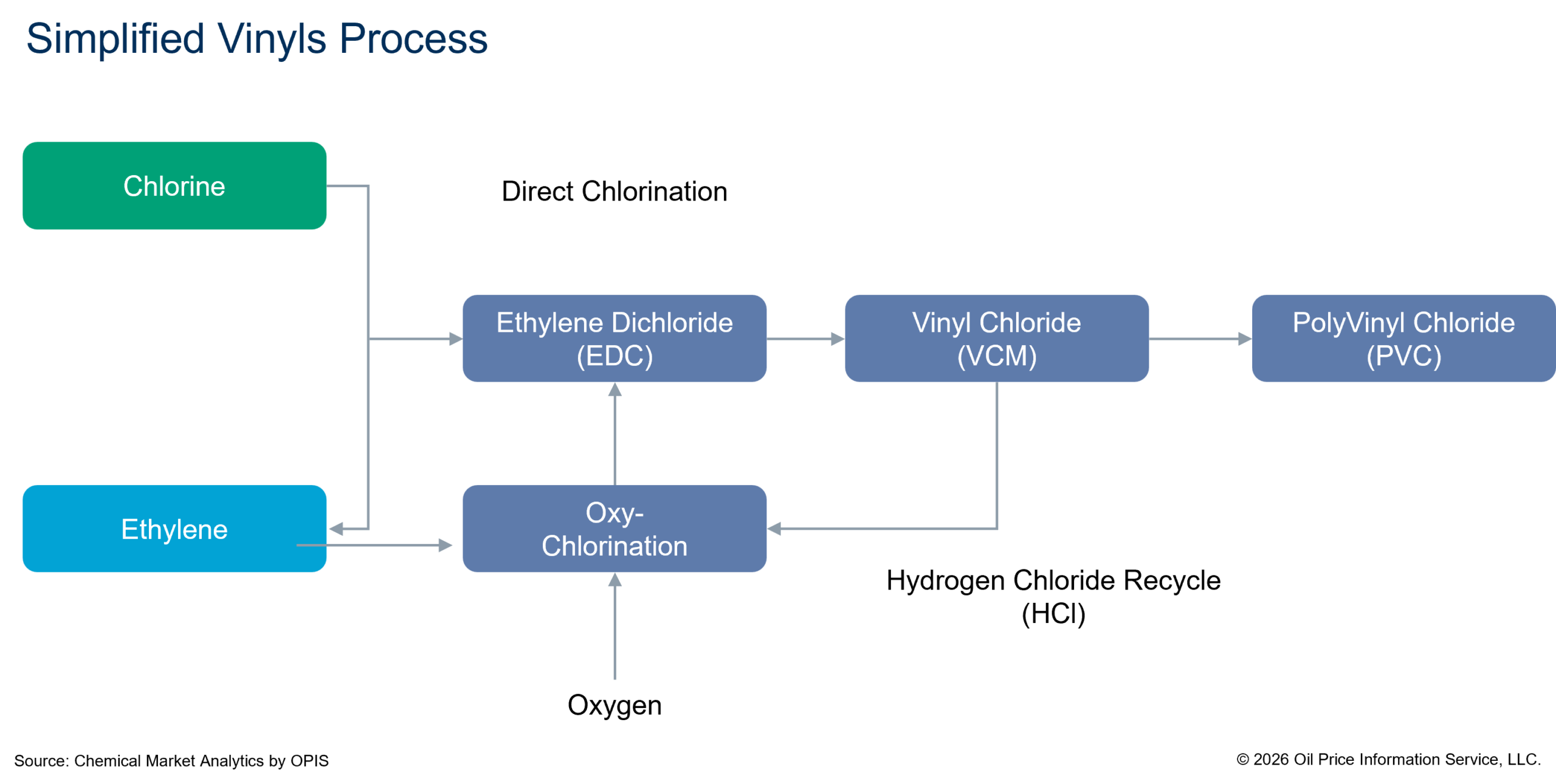

PVC production is a complex, multi-step industrial process that integrates chlorine and ethylene chemistry. In the first stage, chlorine reacts with ethylene to produce ethylene dichloride (EDC) through a process known as direct chlorination.

In the second stage, EDC is thermally cracked to form vinyl chloride monomer (VCM). This cracking process also generates hydrogen chloride (HCl) as a byproduct. The recovered HCl is typically recycled as a chlorine source in an oxychlorination process, where it reacts with ethylene and oxygen to produce additional EDC.

Most modern PVC manufacturing facilities operate balanced plants, which combine direct chlorination and oxychlorination to maximize chlorine efficiency and minimize waste. In the final stage of production, VCM is polymerized to produce PVC resin, which is then supplied to downstream fabrication and compounding markets.

Factors Influencing Price and Price Movement

Commodities are fungible economic goods that the market generally treats as equivalent, regardless of producer. While purchasing decisions may be influenced by established supplier relationships, reliability of supply, or other qualitative considerations, the primary determinant remains the delivered price. PVC is fundamentally a commodity product.

As such, understanding the drivers of PVC pricing and how prices are expected to evolve over a forecast horizon is critical for informed sourcing, sales, and investment decisions. Unlike consumer goods, where prices are often transparent and readily accessible through online platforms or retail promotions, PVC pricing is shaped by a complex set of market forces.

As with all commodities, the balance between supply and demand is a core determinant of PVC prices. Equally important is the industry’s cost structure, which plays a significant role in setting price floors and influencing market behavior. In the PVC market, robust economic expertise and access to detailed data on manufacturing cost inputs are essential for validating current price levels and developing credible forward price forecasts.

Finally, experienced analysts with a long-term perspective on PVC market cycles and deep insight into industry structure bring critical value. Their ability to interpret historical patterns, assess structural shifts, and account for market nuances enhances the accuracy of price assessments and strengthens confidence in forward-looking analysis.

How Cost Structure Influences Price

Global vinyls production is primarily based on two feedstock pathways: ethylene and chlorine, or, in mainland China, carbide and chlorine. As a result, upstream feedstock availability and pricing play a decisive role in shaping regional PVC cash cost structures and global competitiveness.

Across petrochemical value chains, including ethylene and PVC, energy feedstock prices are a critical determinant of production economics. Ethylene is produced predominantly from naphtha, derived from crude oil, or from ethane, which is sourced from natural gas. In mainland China, coal remains the dominant resource for petrochemical production through carbide-based processes. In much of Asia and Europe, petrochemical manufacturing relies heavily on crude oil–based naphtha, while North America benefits from abundant natural gas resources that have underpinned petrochemical feedstock production for decades.

In the United States, approximately 85% of ethylene production is derived from ethane extracted from natural gas. According to the U.S. Energy Information Administration, U.S. natural gas production expanded from roughly 19 trillion cubic feet per year in 2005 to nearly 41 trillion cubic feet by the end of 2024, driven by the development of shale gas. This dramatic increase in supply significantly reduced natural gas and ethane prices relative to alternative petrochemical feedstocks globally, providing North American producers of ethylene derivatives, including PVC, with a sustained cost advantage.

Beyond ethylene, chlorine is the other critical raw material in PVC production. Chlorine is produced from salt (sodium chloride) and electricity, making power costs a key driver of chlor-alkali economics. The U.S. Gulf Coast (USGC) has benefited from structurally low electricity prices since 2009, a shift closely tied to the shale gas revolution. Over the past decade, average natural gas prices in the USGC have been approximately $3.18 per MMBtu, translating into average cogeneration electricity costs of about 3.2 U.S. cents per kilowatt-hour. Given that chlor-alkali production is highly electricity-intensive, consuming well over 2,000 kWh per metric ton of chlorine (alongside roughly 1.1 metric tons of caustic soda), this energy cost advantage materially lowers PVC production costs.

Market Advisory Service – Global Vinyls

Stay ahead with reliable price forecasts, supply/demand data, and strategic industry analysis

Salt availability further reinforces this competitiveness. The United States is the world’s second-largest salt producer after mainland China, with domestic production estimated at approximately 40 million metric tons in 2024, according to the U.S. Geological Survey. Texas and Louisiana rank among the top-producing states and together host more than 80% of U.S. chlor-alkali and vinyls production capacity. The chemical industry accounts for approximately 39% of total U.S. salt consumption, with brine comprising about 91% of the salt used as a chemical feedstock. Chlor-alkali producers are the largest consumers within this segment. An abundant, low-cost salt supply therefore contributes directly to lower chlor-alkali and PVC production costs. Access to competitively priced ethylene, electricity, and salt consistently positions PVC producers toward the lower end of the global cost curve.

A common question is whether tracking crude oil or natural gas prices alone is sufficient to understand PVC price movements. The short answer is no. While feedstock prices are important, PVC pricing is ultimately determined by broader commodity market dynamics. Manufacturing cost structures define competitiveness, but sustainable pricing must also support adequate producer margins to enable reinvestment and long-term supply reliability.

In a market-driven economy, the marginal, or highest-cost, producer required to satisfy global demand effectively sets the price. Because PVC is a fully fungible commodity that moves readily across regions, the highest-cost-producing region typically sets global price benchmarks on a freight-adjusted basis. Consequently, resin buyers and market participants must maintain visibility into international PVC market conditions, rather than focusing solely on local or regional developments, to make informed tactical and strategic decisions.

The Effect of Supply and Demand on Current Price and Price Forecasts

Beyond robust econometric cost models, expert market analysts bring a deep understanding of underlying supply–demand fundamentals and systematically integrate these insights into forward-looking market forecasts. An objective, unbiased assessment of commodity markets provides a balanced view of prevailing supply and demand forces at any given point in the cycle. In evaluating PVC market conditions, analysts assess a broad set of indicators, including industry operating rates, inventory levels and days of supply, shifts in domestic sales, and changes in export volumes. These core metrics are further supported by analysis of competing polymers, evolving consumer preferences, sector-specific outlooks, and macroeconomic drivers such as GDP growth, population trends, and demographic dynamics. Together, these elements underpin Chemical Market Analytics’ quarterly supply–demand balances. Our supply–demand balances represent a structured assessment of petrochemical derivative market fundamentals over time, across multiple geographic levels, including country, regional, and global. Future market developments are forecast using a combination of known events, such as announced capacity additions or closures, and established historical relationships. Long-term balances provide detailed demand breakdowns by derivative and, for PVC, by end-use sector. On the supply side, production is analyzed by feedstock, with historical inventory movements fully accounted for. Demand growth is modeled using GDP elasticity, defined as the ratio of demand growth relative to GDP growth. This approach assumes that macroeconomic expansion, particularly in construction and other PVC-intensive sectors, drives demand for end products. Elasticity assumptions vary between developing and mature economies to reflect structural differences in consumption patterns. Where projected demand exceeds available supply and imports are constrained, hypothetical capacity is introduced to maintain operating rates at economically sustainable levels. Conversely, negative hypothetical capacity indicates anticipated rationalization of capacity in the region. Because PVC, vinyl chloride monomer (VCM), and ethylene dichloride (EDC) are fully fungible and globally traded commodities, trade flows are balanced globally using both historical data and forward-looking projections aligned with long-term supply–demand fundamentals.

In summary, market balance is a primary driver of commodity price direction. When the market is long, characterized by supply exceeding demand, prices tend to move downward, with future prices expected to be lower than current levels, a structure commonly referred to as backwardation. Conversely, when the market is short, and demand exceeds supply, prices typically trend upward, with future prices higher than spot levels, a condition known as contango. In periods of balanced fundamentals, prices generally remain stable and track incremental cost changes until disrupted by unforeseen events that shift the supply–demand equilibrium. Experienced market analysts are uniquely equipped with the tools, data, and judgment required to identify early signals of such disruptions and incorporate them into timely, actionable price forecasts and market analysis.

Conclusion: How Price is Evaluated, and Price Forecasts are Generated

PVC price movements cannot be reliably understood by simply tracking headline crude oil prices or fluctuations in natural gas costs reflected on electricity bills. Instead, PVC pricing reflects the interaction of regional and global supply–demand balances within the broader context of international market dynamics. Chemical Market Analytics’ PVC price assessments are grounded in a rigorous, market-driven discovery process. Our analysts actively engage both buyers and sellers across the value chain to establish a representative, transparent view of monthly price movements in North America, South America, Europe, the Middle East, and Asia, including mainland China.

Looking ahead, our price forecasts are deliberately independent and non-biased. They do not reflect a seller-driven outlook that assumes persistently rising prices, nor a buyer-driven view that expects continuous price declines. Instead, Chemical Market Analytics applies advanced econometric modeling, extensive historical datasets, and deep market expertise to evaluate PVC cash costs, upstream feedstock linkages, and evolving supply–demand fundamentals. These inputs support robust short-term price forecasts covering the next 36 months, as well as long-term outlooks extending to 2060 across all major regions. Long-term forecasts are developed with reference to historical petrochemical cycles and include assessments of projected regional returns on investment for PVC producers. The value of this expert analysis lies in delivering realistic, data-driven price assessments and forecasts, supported by coherent and integrated supply–demand analysis across the upstream and downstream value chains.

For buyers, access to expert market intelligence enables more informed procurement decisions, earlier identification of buying opportunities, stronger sourcing strategies, and the ability to build trusted, long-term supplier relationships. For sellers, independent analysis and forward-looking forecasts provide critical insight to inform internal planning, communicate realistic market expectations to stakeholders, and support sound investment and capacity decisions.

At Chemical Market Analytics by OPIS, we analyze more than 100 commodity chemicals across over 30 specialized market services, extending well beyond PVC. We are a leading provider of data-driven analytics, market intelligence, and price assessments for the global petrochemical industry. Our Market Advisory Services represent one of the most comprehensive resources available, delivering historical, current, and forecast spot and contract pricing, along with near-term market intelligence. These services also provide detailed insights into price discovery dynamics, operating schedules and turnarounds, global trade flows, quarterly supply–demand balances, and the latest developments across all major petrochemical value chains.

For comments and feedback, please reach out to: Ana.Lopez@Chemicalmarketanalytics.com