Petrochemical Feedstocks: The Fundamentals Beyond the Tariffs

By:

- Steve Lewandowski – VP Olefins, Chemical Market Analytics by OPIS

- Pablo Giorgi – Executive Director Olefins, Chemical Market Analytics by OPIS

- Adrian Calcaneo – VP Energy and Feedstocks, OPIS

- Haya Batniji – Principal Analyst Energy and Feedstocks, Chemical Market Analytics by OPIS

Tariff announcements have generated global market turmoil, including in the energy and petrochemical feedstock markets. However, at the time of writing, the effects of the tariffs on feedstocks have generally been limited to lower demand in the short to medium term due to economic fallout and some likely demand rerouting as trade and investment flows shift further down the road.

But even before the onset of the present trade war, petrochemical feedstock market fundamentals were poised to shift in the long term. This piece focuses on the natural gas liquids (NGLs) markets and the structural changes ahead for this sector.

Historical fundamentals: NGLs as a coproduct of oil and gas extraction

The advent of shale gas in North America, especially in the United States, was a game-changer for NGLs production.

NGLs are a coproduct of oil and gas production; a smaller amount is a by-product of refinery operations.

Typically, these would not be produced on purpose for petrochemical feedstock use. Indeed, the first ethylene production unit was built by Union Carbide and Carbon Corporation in West Virginia, United States, in 1921 to convert “useless” ethane and propane, by-products of natural gasoline production from raw natural gas, into more valuable products. This technology laid the foundation for today’s multibillion-dollar petrochemical industry, enabling modern life as we know it.

Notably, the context for heavy barrels was already challenging: In the last few years, the world has been consistently running out of heavy crude. The US Gulf Coast (USGC) refining industry was originally built around domestic light- and medium-quality barrels, as well as around Latin American supply of heavy grades (less than 24o API). These refineries include significant coking capacity, i.e., the technology needed to upgrade low-cost heavy barrels to high-value refined products.

The advent of shale gas in North America, especially in the United States, was a game-changer for NGLs production. In the late 2000s, fracking and horizontal drilling significantly impacted NGL availability and drove down production costs, with abundant, low-cost ethane and propane becoming key petrochemical feedstocks.

Nowadays, NGLs output is still largely determined by oil and gas output and is still considered a by-product of the oil and gas industry. However, most hydrocarbon value chain fixed costs come from building the necessary infrastructure to bring NGLs to market.

The NGLs stream extracted from raw natural gas is typically called the y-stream, a mix of ethane, propane, n-butane, isobutane, and pentanes, which are then pipelined and separated by fractionation in a distillation unit. A subset of NGLs is liquid petroleum gas (LPG), a blend of propane, n-butane, and isobutane. Among NGLs, ethane has the largest share of field production, followed by propane; together they typically amount to 70% of the NGLs volume per barrel.

Because of its physical properties, the NGLs stream can be added to heavy crude as a diluent to make its pipeline transportation more efficient. As such, the NGLs value is linked to the crude value. NGLs separation economics also depend on the natural gas value: Recovery of NGLs may not be economically attractive if the frac spread (=price of purity NGLs – price of natural gas) is too low to cover transportation costs.

In turn, the price of purity NGLs is heavily linked to the chemical industry, as these are used as petrochemical feedstocks, especially ethane and propane, a sector poised to grow as a key demand driver for these products in the long term.

Global Ethane Outlook

The Ethane Edge: Intelligence that Powers What’s Next

NGLs as petrochemical feedstocks: ethane and propane

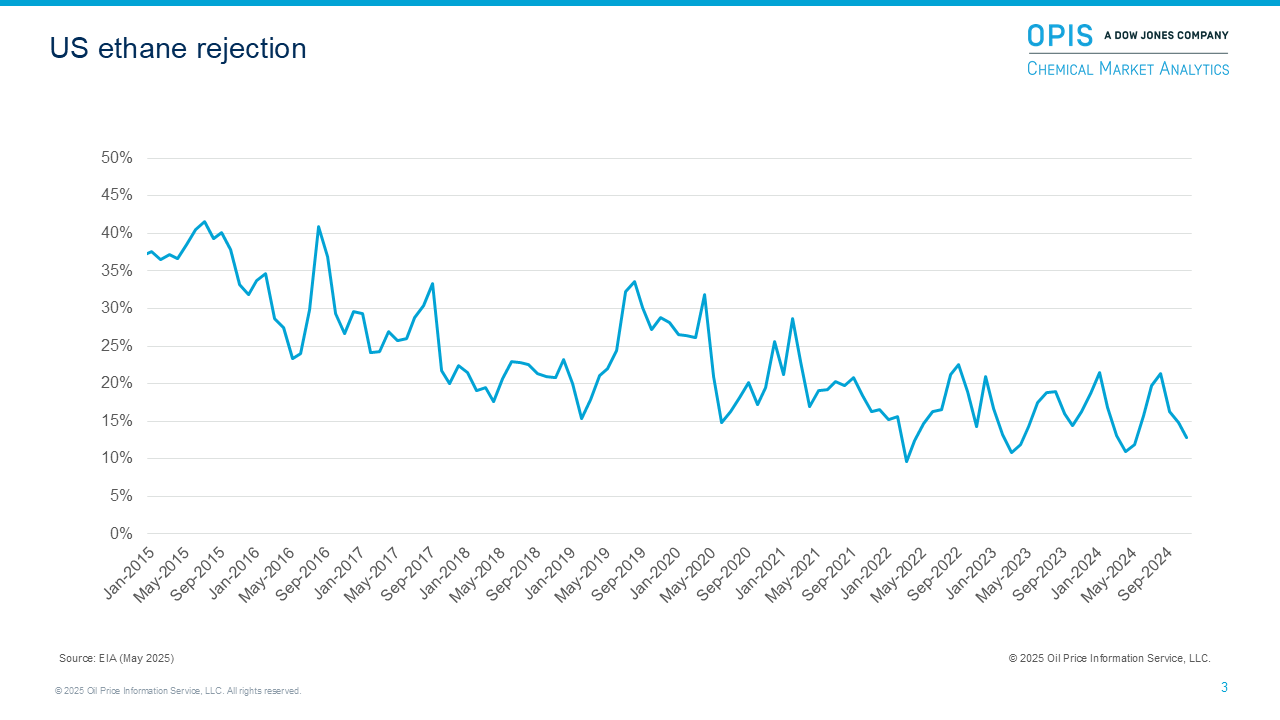

Most ethane is left in the natural gas mix or recovered for petrochemical feedstock for ethylene production; the latter is typically directly supplied to consumers (point-to-point delivery).

When ethane prices are low, the volumes can be rejected, meaning the ethane is left in the natural gas stream, contributing to domestic and industrial natural gas consumption, power generation, etc.

That said, some ethane must be recovered from the natural gas stream to ensure the heat energy level remains within the safety limit for public consumption in urban areas. As a result of variable rejection based on extraction economics, the ethane composition in the y-stream might change over time.

Notably, all non-rejected ethane is further processed into petrochemicals, with ethane being the top global feedstock for ethylene production, a major building block of the chemical industry.

Meanwhile, most propane is a by-product of oil and gas processing, but significant production also comes from refineries. Propane has a high heat content, so it must be extracted from natural gas for public consumption. Using it as a petrochemical feedstock was a solution to manage excess, but propane is used in multiple other sectors.

Within the petrochemical sector, propane is mainly used as a feedstock for light olefins production, i.e., ethylene and propylene, both major building blocks for the chemical industry. While propane is an important petrochemical feedstock, a significant share of its demand comes from residential and industrial sectors, particularly for heating and power. These segments often influence market direction more than chemical use. When temperatures drop or export activity increases, propane prices typically rise, limiting availability for petrochemical applications.

When that happens, petrochemical producers often shift to using naphtha. Although naphtha is generally more expensive and less targeted for light olefins production, it remains a viable alternative. It is well-integrated into the existing steam cracker infrastructure and provides a wider range of coproducts. As a result, propane is preferred when it is competitively priced, but naphtha plays a key role when propane loses its cost advantage.

Light olefins such as ethylene and propylene are key base chemical markets, each respectively amounting to 188 million metric tons and 125 million metric tons produced in 2024. These products are used in a plethora of downstream chemical derivatives, which in turn end up in most everyday goods. By far, the largest demand sector for ethylene is polyethylene (PE) and for propylene it is polypropylene (PP).

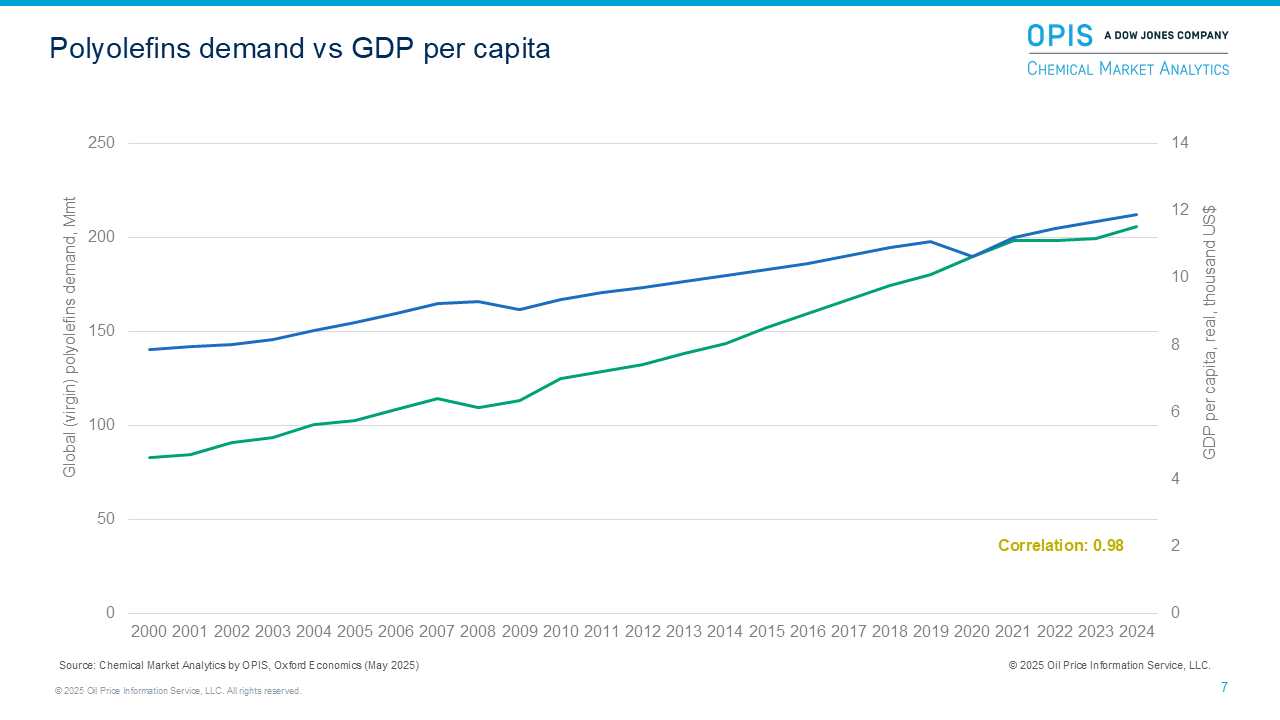

Polyolefins improve standards of living

Polyolefins overtake all other polymers in market share of both durable and nondurable plastics demand by volume. The first commercial-scale PE plant started up in 1939, and commercial PP production began in 1957. Since then, PE and PP use has grown exponentially, touching a wide range of goods used in everyday life, with global (virgin) market sizes reaching 120 million metric tons and 87 million metric tons in 2024, respectively. Today, about 43% and 12% of PE is used for consumer packaging and consumer goods and appliances. Meanwhile, 37% of PP is used in consumer goods and appliances, and 31% goes into medical and personal care applications.

PE and PP have revolutionized standards of living; unsurprisingly, polyolefins demand is projected to continue growing through 2050. Both PE and PP are forecast to grow at an over 2% average annual growth rate (AAGR) in 2024–50, largely linked to forecast population growth and improving GDP per capita and consumer spending in emerging economies.

Despite growing recycling trends, virgin polyolefins demand is still projected to grow by 85% between 2024 and 2050; feedstock supply will have to meet this added demand. This could be particularly challenging in a world where the general aim is to phase out fossil fuels within the next few decades.

Long-term olefins feedstock balance changes: Key drivers

Retrofitting Asian naphtha crackers to flex-feed could tighten the ethane market

Ethane prices are currently particularly low compared to other feedstocks. This gives ethane-feed ethylene producers a clear advantage, especially in the United States and Middle East.

However, ethane’s affordability is also incentivizing Asian ethylene producers to retrofit existing naphtha-based crackers to flex-feed crackers that can use ethane or even incorporate this flexible optionality into new assets. This trend has become especially prominent in the current petrochemical environment, where ethylene production margins are very low, if existent, for most of the world, and ethane flex-feed crackers could offer some relief to those who convert.

Notably, there are risks to making the switch. For one, there is not an infinite supply of ethane, so in the event of growing demand from the conversion of liquid feed assets to flex-feed, the relatively low price historically associated with ethane compared to alternative feedstocks could quickly change.

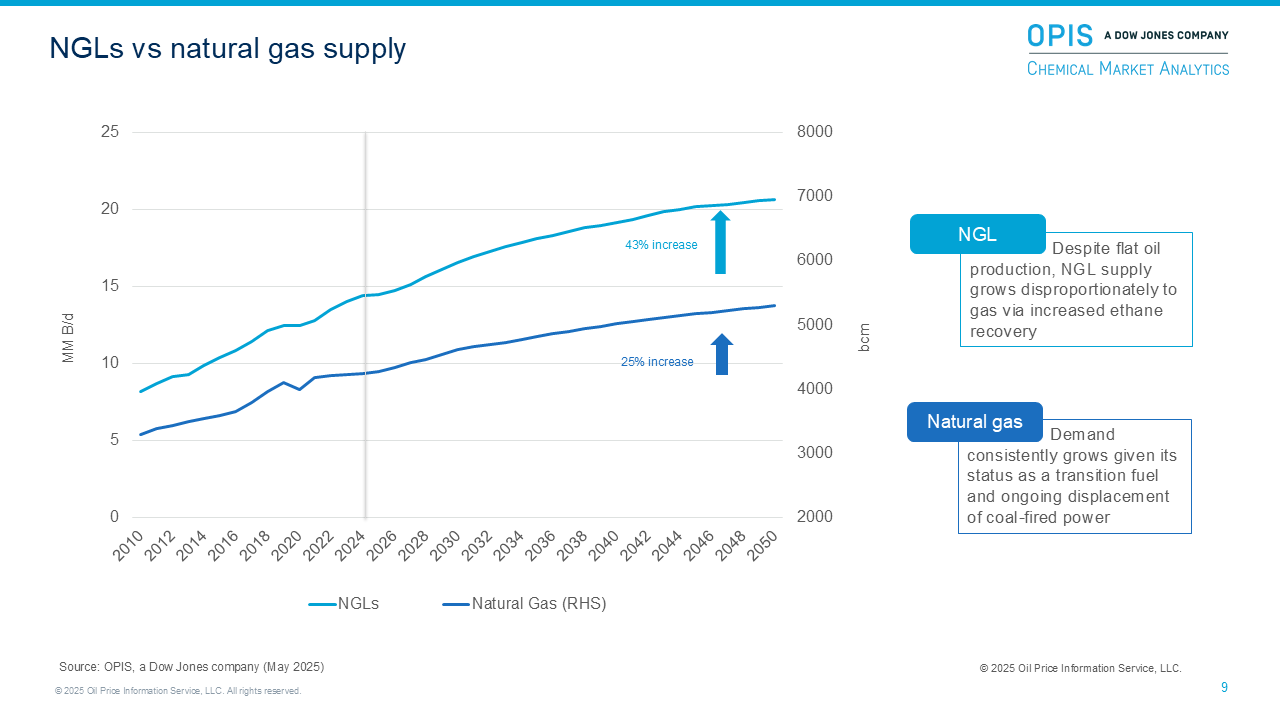

Overall, in the long term, the petrochemical sector’s appetite for light feedstocks will grow, positioning ethane/propane consumption for sustained growth. This means that purity NGLs prices will likely increase, at least until more capacity comes online—but new projects will have to overcome significant hurdles.

Ethane’s affordability is also incentivizing Asian ethylene producers to retrofit existing naphtha-based crackers to flex-feed crackers that can use ethane or even incorporate this flexible optionality into new assets.

Constraints to new NGLs capacity: Infrastructure costs and the energy transition

One major bottleneck for new NGLs extraction capacity is typically transportation and storage economics. As these are mixtures with low density and low viscosity that require fairly high pressure and low temperatures to remain liquid, NGLs transportation costs plays a significant role in project economics.

To bring additional NGLs volume to market, significant infrastructure investment is required:

- After the y-stream is extracted from the liquid-rich natural gas stream, it will be pipelined to a fractionator to be split into purity NGLs.

- Storage of the y-stream and purity products is also typically required.

- More pipelines can potentially be added downstream for direct supply to domestic consumers and/or export terminals.

- Jetties are often required for ship or barge delivery loading.

- If an asset has an export focus, a fleet of ships will be required to ensure steady supply to customers.• Finally, if they arrive via seaborne vessels, investment is also required on the receiving end of these products, including jetties, storage. and pipelines.

Another major hindrance for new NGLs output is the energy transition: Less oil and natural gas production could lead to scarcer NGLs supply as a crude oil extraction by-product. Conversely, natural gas will still be seen as a transition fuel to displace coal in power generation, so that will likely be supportive of more projects in this space.

Future fundamentals shift: On-purpose feedstocks

A tighter NGL purity market could provide sufficient incentive to extract more of these petrochemical feedstocks at conveniently located assets and might even support new investment. Additionally, new ethane sources could rise to meet the supply gap from growing petrochemicals demand: NGLs capacity could potentially be added in Russia, Argentina, etc.

In the context of a tightening feedstocks market, selectivity may still be desirable for ethylene and propylene production. This means that despite rising ethane and propane costs, strong petrochemicals demand growth could be supportive of on-purpose ethane/propane production, albeit at a higher cost. With that in mind, our long-term outlook expects the NGLs supply to grow almost twice as much as natural gas by 2050.