Impact of US-Israel Conflict with Iran: Olefins and Polyolefins

Experts:

- Matthew Thoelke, Vice President, EMEA Olefins

- William Chen, Vice President, Asia Olefins

- Pablo Giorgi, Vice President, NAM Olefins

- Joel Morales, Vice President, NAM Polyolefins

- Kaushik Mitra, Executive Director, EMEA Polyolefins

- Alan Wei, Executive Director, China Polyolefins

EMEA

Middle Eastern Supply Shocks

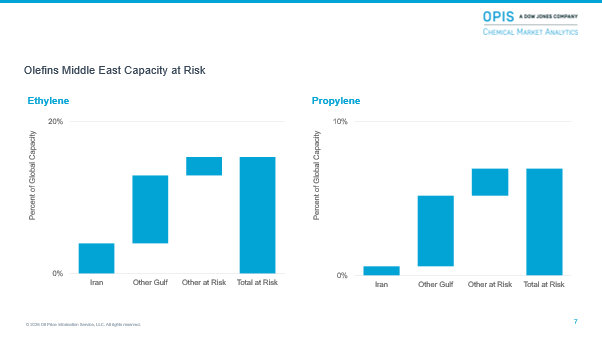

More than 15% of global ethylene and nearly 7% of global propylene capacity is in the region affected by the conflict. Most Middle Eastern Gulf capacity is located outside of Iran, especially propylene capacity. Feedstock supply issues and export constraints were initially the main obstacles to producers, dramatically increasing inventory levels. However, attacks in early April have resulted in an almost complete cessation of operations for middle East Gulf operators.

In addition to crude oil, liquefied natural gas (LNG), liquefied petroleum gas (LPG), and naphtha, the Middle East exports significant volumes of olefins and olefin derivatives, at 6% of global ethylene exports and 30% of global polyethylene (PE) exports. The closure of the Strait of Hormuz, the main route for exports from the region, along with strikes in Oman and fear of attacks by Yemeni-based Houthi rebels in the Red Sea is ensuring a high level of risk across the region. A dramatic portion of global ethylene capacity is exposed as a result, with a more moderate level of propylene at risk.

At the time of writing, Middle Eastern ethylene and derivatives production has already been significantly affected due to upstream force majeures and supply chain limitations. European PE production is stable but facing high raw material and energy cost inflation. Demand is being fueled by restocking, but buyer resistance to price increases is growing, with significant risk of negative margin elasticity in the coming weeks.

Output disruptions in the Middle East are already affecting over 70% of polyethylene (PE) and polypropylene (PP) capacity in the region at the time of writing. European PE and PP production is stable, but higher costs will press margins. Import restrictions lie ahead for Europe, but also for Turkey and Africa. Restocking is ongoing, but sharp price increases will affect buying in the coming weeks. Ultimately, consumer discretionary spending is expected to decrease if inflationary pressures persist.

The Strait of Hormuz is critical to Middle Eastern exports, especially into Asian markets and Southern Africa. There are also significant export flows to the European and north African markets; these flows may be partly maintained through the Suez Canal, due to port constraints and security risk through the Bab-al-Mandab Strait. PE and monoethylene glycol (MEG) are most at risk of direct impacts. Considerable concerns are developing in many Asian countries, particularly with respect to fuel security, but also to petrochemical availability.

The conflict has already resulted in damage to assets and centralized utilities at regional olefin production sites, causing major disruptions and likely long-term unavailability. Additionally, several assets are close to completion in Iran, and the likelihood of these units being finished soon is very low.

Elsewhere in the region, new capacity is close to completion in the United Arab Emirates, Qatar, and Saudi Arabia, and progress is likely to be affected as EPC (Engineering Procurement & Construction) resources get stretched. Progress on additional new projects under consideration in the region is likely to face greater challenges as geopolitical risk premium remain elevated impacting long term return assessments.

European Price Correction Lags

One critical factor for European markets is the delayed price correction inherent in the European olefins contract mechanism. With the price set ahead of the period in question, it is not possible to quickly respond to volatility.

In historical periods of price volatility, sharp upward moves in feedstock prices squeezed cracker margins, in some cases for multiple months, while downward corrections in oil prices boosted margins to extremely high levels. The March 2026 upward pressure on oil and naphtha has pushed European naphtha cracker variable margins into negative territory. The position is not as severe in April, though margin compression continues to be seen for European operators.

The European ethylene market faced several supply constraints in March due to multiple planned and unplanned disruptions. Despite dramatic upward moves in price, there is still strong prompt demand, as buyers are preparing for growing limitations in imports and constraints in European supply.

At the time of writing, no supply relief is anticipated in the short-term, ensuring the market will remain tight in the coming weeks. During the second half of March, elevated energy and feedstock costs caused most producers to operate at negative variable margins. As a result, spot prices surged significantly, varying by location and urgency. Further rises in crude oil and feedstock prices have left producers with challenged economics despite the record increase in the April contract prices.

Asia

Cracker Operations and Economics

The current situation’s impact on olefin producers varies. Some producers may face challenges, while others could benefit, and some may experience a mix. The timing of the impacts also differs.

Even prior to the conflict, escalating tensions had pushed crude oil and chemical feedstock prices higher since January 2025, leading to reduced operating rates for naphtha-based crackers in Asia. The subsequent spike in crude oil and feedstock costs has only intensified the pressure on Asian producers, further challenging margins and operational flexibility.

Standalone steam crackers in Asia that rely on imported naphtha and LPG from the Middle East are currently under significant pressure. Even integrated refinery-cracker complexes, which typically enjoy more secure feedstock access, are not immune. If their crude oil supply comes from the Middle East, the entire refinery-cracker operation will face heightened vulnerability.

As a result, both standalone and integrated crackers must adapt quickly. Some producers are reducing operating rates, considering short-term shutdowns, or advancing planned maintenance turnarounds to mitigate feedstock risks. In addition, several operators are evaluating the possibility of declaring force majeure.

Methanol-to-Olefins

Methanol-to-olefins (MTO) production in mainland China has been heavily disrupted by the ongoing geopolitical crisis. Inland MTO plants that source methanol from domestic coal-to-methanol (CTM) facilities are relatively insulated, while coastal units dependent on Middle Eastern imports, especially from Iran, are more vulnerable to feedstock shortages. However, the relative cost position compared with other olefins production processes is a moving target, as rising production costs are not limited to the MTO sector. MTO economics and future operating rates are expected to remain dynamic.

In 2025, around 70% of mainland China’s methanol imports came from the Middle East, with Iran supplying more than half of the volumes used by MTO producers. About two-thirds of China’s MTO capacity is in coastal regions and relies heavily on imports. As most Iranian cargoes transit the Gulf and the Strait of Hormuz, a prolonged closure would effectively cut off supply to mainland China’s coastal MTO infrastructure. However, there are alternatives: at the time of writing, MTO operators have increased methanol sourcing from domestic coal-to-methanol facilities, supported by a modest recovery in operating rates.

Propane Dehydrogenation

Asian propane dehydrogenation (PDH) capacity outside of mainland China is comparatively small. In South Korea, PDH producers predominantly source propane from the US, so their operating decisions are more likely to be margin-driven rather than linked to feedstock shortages. In contrast, PDH units in Southeast Asia may face greater pressure from supply constraints, as most of their propane has traditionally been sourced from the Middle East.

If the Strait of Hormuz were to remain closed for an extended period, PDH producers would need to turn to alternative supply sources that might not be readily available and would most likely be more expensive. For PDH producers in mainland China that want to increase US propane imports, additional tariffs would raise costs further, making this option less immediately attractive.

Meanwhile, higher crude oil and LPG prices across Asia have pushed PDH production costs up, putting many plants at the upper end of the regional cost curve. Constrained feedstock supply and elevated energy costs have led several facilities to reduce operating rates, squeezing margins and limiting operational flexibility. Some producers are adjusting production schedules, seeking alternative LPG sources, or exploring short-term contracts to stabilize supply.

Potential Gains

Advantages may stem from access to lower-cost feedstocks, operational flexibility, diversified supply chains, or strategic geographic locations that allow participants to navigate disruptions more effectively than their peers.

Such producers might include:

- Southeast Asian integrated refinery-steam crackers that source offshore crude: Offshore drilling carries a higher extraction cost but is shielded from market volatility. Internal transfer pricing provides a significant competitive edge over standalone competitors.

- Northwest China: Operators using crude from mature domestic fields, decoupled from high international spot prices, saw integrated margins improve due to derivative price increases.

- Ethane Cracking: Steam crackers using US imported ethane have stable feedstock costs. Mainland China and India are the only two Asian markets that import US ethane, but the current crisis should prompt more Asian producers to do so. Local ethane in Southeast Asia and mainland China is also supporting operators’ margins.

- CTO: This sector in mainland China has been a primary beneficiary of the crisis and is currently highly profitable, as coal costs are relatively stable, making investments more attractive.

- Russian Feedstock Arbitrage: Discounted crude oil and chemical feedstocks imported from Russia have remained competitive, namely in mainland China and India.

Short- and Long-term Implications

In the immediate term, Asian olefin producers face heightened pressures from rising crude oil and feedstock prices. Supply chain disruptions, elevated freight costs, and insurance premiums are adding further strain, while volatility in downstream derivatives and methanol are complicating planning and inventory management. In the short term, producers are adjusting production schedules, optimizing logistics, actively managing inventory, and seeking alternative suppliers where possible to maintain operations and mitigate immediate cost pressures.

Market Advisory Services

Stay ahead with reliable price forecasts, supply/demand data, and strategic industry analysis

PE production will remain subdued due to feedstock availability issues until the supply chain normalizes by 2027. Even if the conflict had ended by end-March, demand destruction would last until mid-2026. Meanwhile, stalled LPG supplies will weigh on PP production, particularly from PDH-PP assets. The biggest impact will be on discretionary product sales due to higher inflation and likely higher lending rates in many countries.

Over the medium to long term, the conflict is expected to reshape the strategic landscape. Companies are likely to diversify feedstock sourcing, invest in dual-feedstock capabilities, expand storage and regional integration, and secure long-term supply agreements. Sustained higher energy costs could widen the competitive gap between US ethane-based producers and Asian naphtha-based producers, influencing trade flows, capacity decisions, and plant economics. The crisis is likely to accelerate the energy transition in several Asian countries, especially when aims are closely tied to enhancing energy via less reliance on imported fossil fuels.

North America

US Capacity to Replace Middle Eastern Ethylene and Derivatives Supply Gap

With Middle Eastern exports effectively closed off, Northeast Asia, India, and Europe have been unable to import sufficient steam cracker feedstock volumes to make ethylene, import ethylene, or import ethylene derivatives to make finished products. The US has limited ability to export incremental volumes of LNG, LPG, and ethylene, but it does have the capacity to export more derivatives. If global commodity prices increase and those arbitrages open, US producers will increase exports to capitalize on those netbacks. There is enough spare capacity in the US to increase PE, ethylene oxide (EO), and ethylene dichloride (EDC) production.

US steam crackers are currently operating at high rates, limiting incremental ethylene availability from crackers, assuming domestic demand for derivatives remains stable. Notably, the US has near-record ethylene inventory caused by weak derivative demand and high cracker operating rates in 2025, which could support increased ethylene demand for a few months. However, a sustained demand pull would cause ethylene inventories to plummet, placing upward pressure on domestic prices and prompting domestic demand destruction. Therefore, the US could temporarily replace some of the ethylene derivative volumes that are short but cannot supply both its domestic markets and expand its exports long term.

With local ethane and natural gas prices largely unaffected, North American PE production is expected to increase in the short term to support higher exports. Margins are spiking, and the industry’s profitability outlook has dramatically changed for 2026 and potentially beyond.

Regional Pricing Expectations

We forecast that North American ethylene prices will remain elevated throughout Q2 2026.As production facilities in other regions shut down due to unfavorable economics, North American producers are ramping up ethylene derivative exports to fill the global gap. Limited domestic capacity will further constrain supply, likely pushing North American prices to new highs.

Meanwhile, rising naphtha prices have forced many global steam crackers to reduce rates or shut down entirely. While most US producers use ethane, which is less sensitive to the 2026 conflict, the resulting global supply tightening is putting upward pressure on domestic prices.

US Capacity to Replace Middle Eastern Propylene and Derivatives Supply Gap

Total PP production potentially at risk in the region is approximately 8% of global demand. In 2025, the Middle East accounted for 7% of global propylene and 27% of global PP exports, mainly to West Europe, North Africa, the Indian subcontinent, and Asia. Beyond the halt of propylene and derivative exports, it will be more difficult for other regions to import the propane necessary to produce propylene and downstream finished goods. This has created significant upside potential for propylene demand in the US. Middle Eastern export constraints have created favorable arbitrage windows, allowing for more US PP production to partially satisfy emerging gaps.

Average PP operating rates in the US have hovered around 75% over the last two quarters due to soft downstream demand; if domestic PP utilization climbed to a technical maximum of 90%, it could, in theory, cover approximately 20–25% of total Middle Eastern net exports. However, actual output will also be determined by feedstock costs and margin viability. If propane and propylene prices become cost-prohibitive, producers may cap operating rates despite global PP demand to avoid margin compression.

For now, several propylene derivatives have already increased rates to meet international demand, including PP, meaning propylene inventories will continue to decline. PP production margins are rising, and the industry’s profitability outlook appears to be improving for the full year. That said, domestic propylene supply remains constrained.

Steam crackers are running at very high rates, and units currently offline are down primarily due to maintenance turnarounds. After these units resume production, there still won’t be enough propylene to meet the incremental demand for derivative exports. After the first two months, we expect that propylene inventories would fall, and prices would rise to curb incremental derivative exports. Additional propylene could come from refineries, but the cost is not only very high, it’s also a moving target, as it is competing in various ways with gasoline production.

World Analysis

Obtain Supply/demand, capacity and price, cost, and margin databases provide forecasts up to 2060.

Effect on Domestic Propylene Prices

Propylene spot prices in Mont Belvieu have been increasing since the start of the conflict. Inventories keep decreasing, putting additional pressure on prices. While North American costs are up, they have not increased as much as in the rest of the world.

At the time of writing, our baseline forecast assumes eight weeks of armed military conflict, but the impact on oil, gas, feedstocks, and supply chain normalization will last much longer. If export demand persists beyond April, propylene prices will need to increase to disincentivize those exports, effectively closing the arbitrages.