Natural Rubber: Production Shifts, Demand Headwinds, and Emerging Technologies

Introduction

Natural and synthetic rubber are essential raw materials for tire manufacturing, alongside key inputs such as silica, carbon black, reinforcing fibers, steel cord, and specialty chemicals. Global automotive production began recovering in 2021 following the sharp decline caused by the COVID-19 pandemic in 2020; however, growth remained subdued due to persistent supply chain disruptions, particularly those stemming from the Russia–Ukraine conflict.

While auto-parts supply constraints have largely eased, automakers are increasingly facing demand-side pressures driven by U.S. vehicle import tariffs, prolonged high inflation, and elevated interest rates, all of which are dampening consumer purchasing power. As a result, growth in vehicle production has become more uncertain.

The demand for natural rubber is closely tied to the performance of the automotive and tire sectors. Demand has been gradually recovering alongside higher vehicle output and improving replacement tire consumption. Nevertheless, the industry continues to face emerging headwinds, including new trade barriers, ongoing geopolitical risks, and broader macroeconomic uncertainty.

This focus report provides an up-to-date assessment of the global natural rubber market, offering insights into demand trends, supply dynamics, and key risks shaping the outlook for the tire and automotive value chain.

Southeast Asia remains the primary supplier of global natural rubber, although production declines have emerged in several traditional leading producers, including Thailand, Indonesia, and Malaysia, reflecting growing structural and operational challenges across the region.

Production

Global natural rubber production has continued to expand, rising above 14 million metric tons in 2022 and reaching approximately 14.5 million metric tons in 2024. Southeast Asia remains the dominant supplier of global natural rubber; however, output has declined in several traditional producing countries, including Thailand, Indonesia, and Malaysia.

Malaysia’s natural rubber production has been on a sustained downward trend since 2019 and has fallen to below 400 thousand metric tons per year, reflecting structural challenges within the sector.

Indonesia has experienced a particularly sharp contraction in output since the COVID-19 pandemic, driven by prolonged low natural rubber prices, a reduction in rubber processing capacity, and tree disease issues. The pace of decline is notable: Indonesia produced over 3 million metric tons annually between 2012 and 2019, but production has since fallen by more than 35%, raising concerns about long-term supply resilience.

In Thailand, production declined in 2024 due to adverse weather conditions during the first half of the year. As a result, combined output from the two largest producers, Thailand and Indonesia, fell by approximately 3% year on year in 2024, highlighting growing supply-side risks in the global natural rubber market.

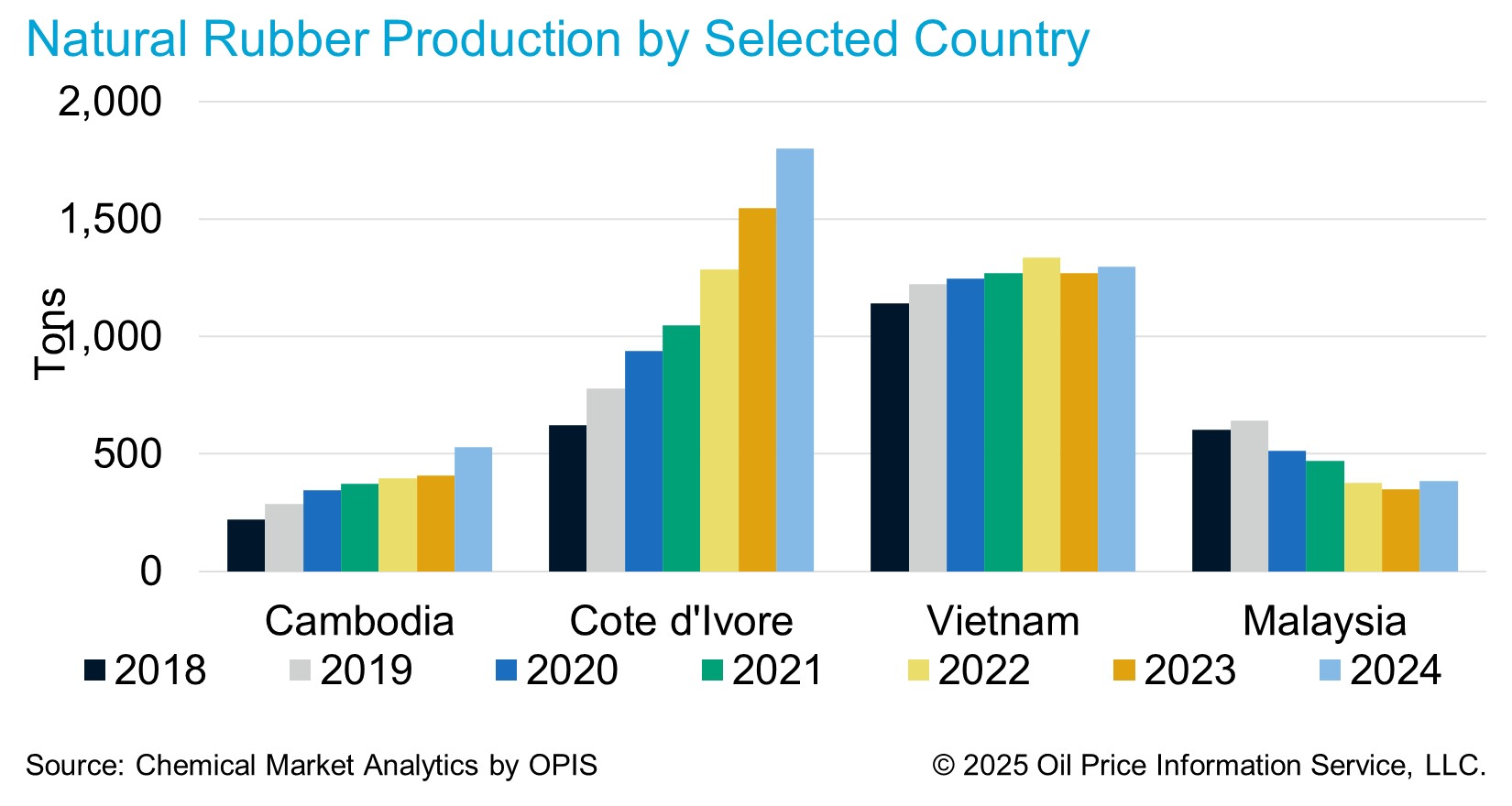

In contrast to traditional producing regions, natural rubber output from non-traditional producing countries has increased significantly, led by strong growth in Côte d’Ivoire. The country has emerged as the third-largest natural rubber producer globally, with production volumes now only slightly below those of Indonesia.

Other emerging producers, including Cambodia, Laos, and Myanmar, have also expanded their output. Combined production from these non-traditional suppliers exceeded 1 million metric tons in 2023, helping to partially offset supply declines in established producing countries. As a result, global natural rubber production increased by approximately 3% year on year in 2024.

Despite this expansion, global production growth is expected to remain marginal in the coming years. Ongoing and potentially accelerating production losses in the two largest producing countries—Thailand and particularly Indonesia—are likely to limit overall supply growth, underscoring persistent structural risks to long-term global natural rubber availability.

Demand

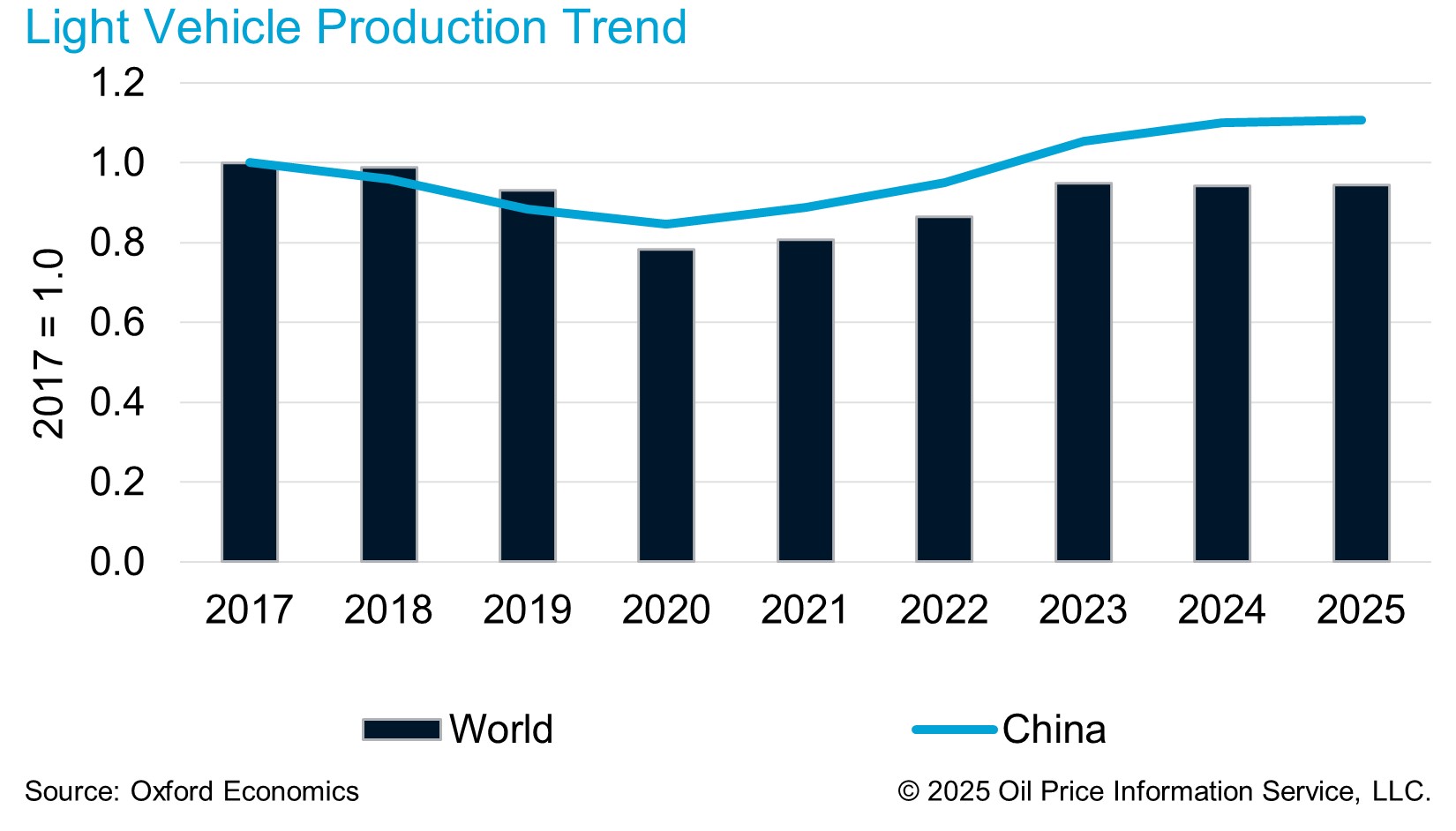

Global light vehicle production has recovered gradually following the severe disruption caused by the COVID-19 pandemic in 2020. Since then, the automotive industry has faced multiple challenges, including persistent supply chain constraints, heightened geopolitical risks, and the ongoing impact of the Russia–Ukraine conflict, all of which have slowed the pace of recovery.

Mainland China has led the global rebound in light vehicle production, supported by strong growth in electric vehicles (EVs) and sustained government policy support. China has already surpassed its 2017 production peak, the highest level recorded prior to COVID-19, while global light vehicle output has only recently exceeded 2019 levels. The primary drivers of post-pandemic production growth have been EVs, which expanded at an average rate exceeding 60%, and hybrid vehicles, which grew by more than 30% on average. In contrast, automakers worldwide have continued to scale back pure internal combustion engine (ICE) vehicle production.

Looking ahead, the automotive sector is confronting new headwinds stemming from reciprocal and sector-specific U.S. tariff measures. While reciprocal tariffs aim to rebalance U.S. trade relationships, sectoral tariffs specifically target industries such as automotive and steel, introducing renewed uncertainty for global vehicle supply chains. As a result, Oxford Economics has revised its global light vehicle production outlook downward, with worldwide output expected to remain flat year on year, reflecting the dampening impact of U.S. trade policy.

These tariffs are expected to affect all major vehicle-exporting countries to the United States, particularly the top five exporters—Mexico, Japan, South Korea, Canada, and Germany—as well as other exporting nations. The resulting trade friction is likely to weigh on production planning, investment decisions, and global automotive supply flows in the near term

Global natural rubber demand grew by approximately 2% in 2024, continuing its gradual recovery following the COVID-19 downturn. Tire demand, the dominant end-use segment for natural rubber, is divided into original equipment (OE) and replacement (RE) markets. OE tire demand has strengthened in line with the recovery in light vehicle production, while replacement tire demand has remained subdued. Reduced vehicle mileage during the COVID period delayed tire wear cycles, resulting in weaker replacement demand.

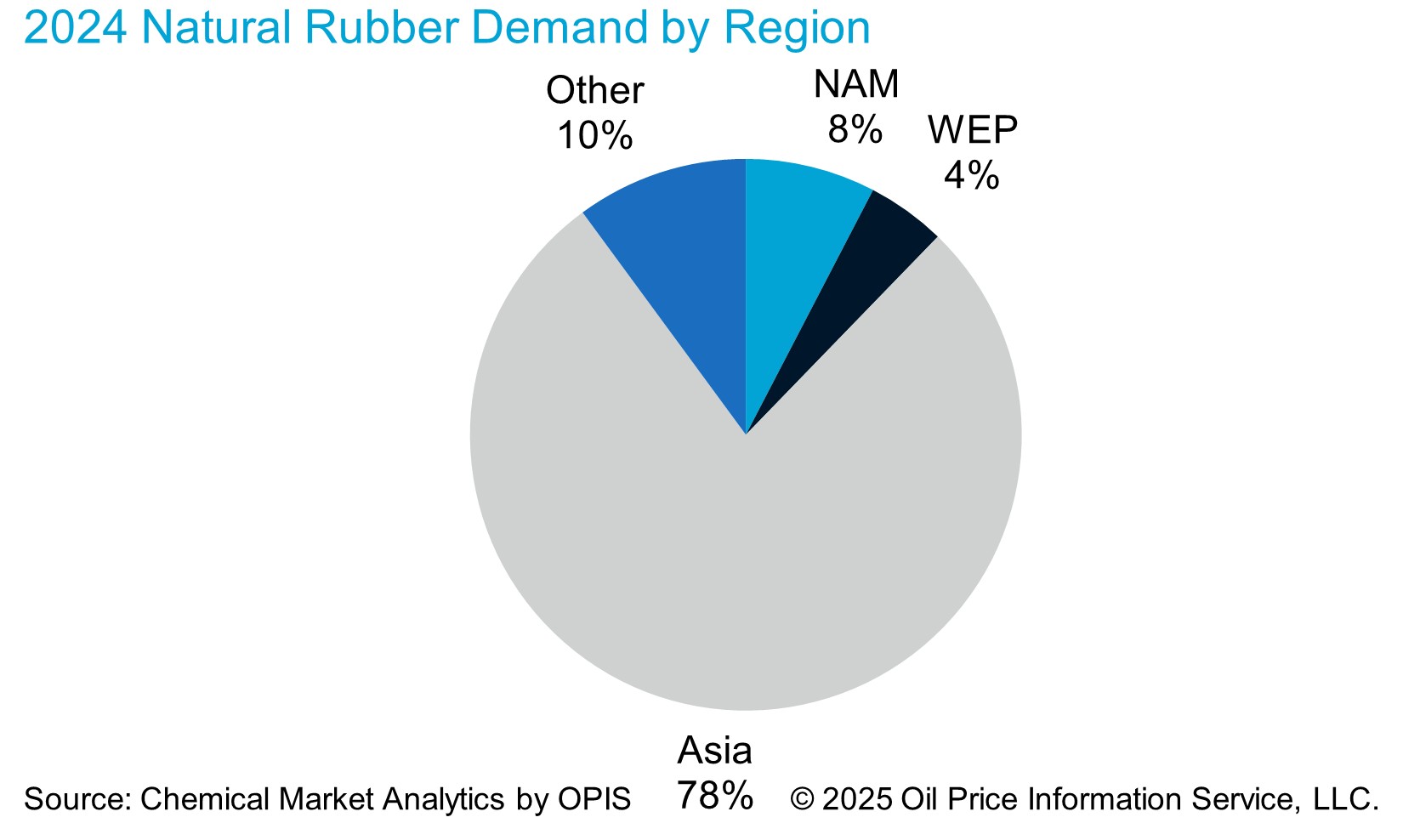

During 2023, elevated tire inventories prompted manufacturers to curtail production in order to rebalance supply. As inventories were gradually drawn down, tire production resumed modest growth in 2024. Global natural rubber demand reached approximately 14.5 million metric tons, marginally below total production, with Asia accounting for the majority of consumption growth.

In contrast, natural rubber demand in Europe has contracted, primarily due to the Russia–Ukraine conflict, which led to sanctions on Russian tire exports within Europe and a subsequent increase in Asian tire imports. Looking ahead, natural rubber demand growth is expected to remain flat, as ongoing tariffs on vehicles and automotive components, combined with broader macroeconomic uncertainty, continue to weigh on tire demand across key regions.

Market Advisory Service: Asia C4 Olefins & Elastomers

Stay ahead with reliable price forecasts, supply/demand data, and strategic industry analysis

New tapping technology

In mainland China, the Chinese Academy of Tropical Agricultural Sciences (CATAS) has introduced an AI-powered rubber-tapping robot, marking a notable technological advancement in natural rubber harvesting.

The robot is equipped with a multi-degree-of-freedom robotic arm and caterpillar-track mobility, enabling it to navigate complex plantation terrain. Using AI-driven sensing and control technologies, it can adjust to variations in tree bark thickness and cutting angles, delivering precision cuts while maintaining latex quality.

The system achieves approximately 80% of manual tapping efficiency, with the capacity to harvest 100–120 trees per hour and operate continuously for over eight hours on lithium battery power.

The estimated cost of the rubber-tapping robot exceeds RMB 100,000 (approximately USD 14,000). At this price point, adoption is likely to be limited to large-scale plantations, particularly those facing acute labor shortages. The technology is currently less viable for smallholder farmers, who account for approximately 75–80% of global natural rubber production.

While large plantations may leverage automation to stabilize yields and mitigate labor constraints, broader adoption across the natural rubber sector will depend on further cost reductions. Lower equipment costs would be essential for smallholders to integrate robotic tapping solutions into their production systems and sustain long-term supply growth.