Implications of Changes in Mainland China’s VAT Refund Policy on the Polyether Polyols Market

Polyols Export Policy Overview

In January 2026, the Ministry of Finance and the State Taxation Administration of China made a surprise announcement on the cancellation of the Value-Added Tax (VAT) refund on exports of photovoltaic and related products. The new policy is set to take effect from 1 April 2026 and polyether polyols are included within the range of products. The unexpected move immediately sparked panic buying of the affected products and raw materials ahead of the policy’s implementation. The removal of the VAT rebate increases the cost of polyols exports for mainland Chinese producers and marks a structural shift in the pricing economics of the global polyether polyols market.

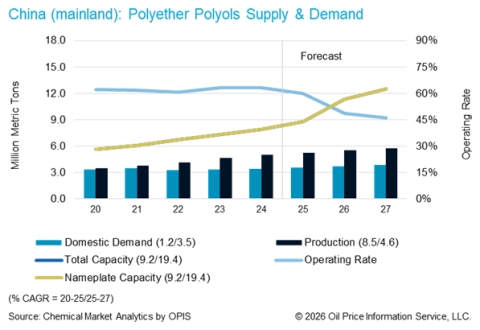

Historically, VAT refunds provided a significant cost advantage to polyols export companies from mainland China, particularly for heavily oversupplied polyether polyols (see chart 1.1). With mainland China accounting for the majority of incremental global capacity additions in recent years, exports have been critical for absorbing excess volumes. The policy change therefore directly affects the world’s largest supplier and the regional price setter.

Trade and Market Implications

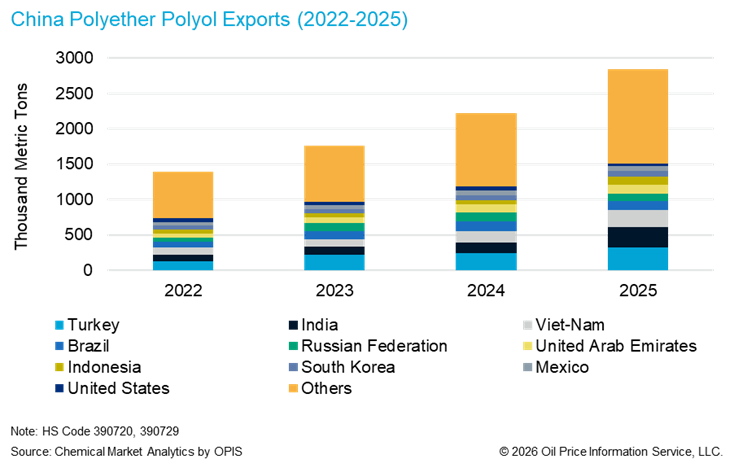

According to Global Trade Tracker, mainland China is the world’s largest exporter of polyether polyols. Exports rose from 1.7 million tons in 2023 to 2.8 million tons in 2025, reflecting rapid expansion in domestic capacity. Key export destinations include Turkey, India, and Vietnam, all of which are highly dependent on mainland Chinese-origin materials (see Chart 1.2).

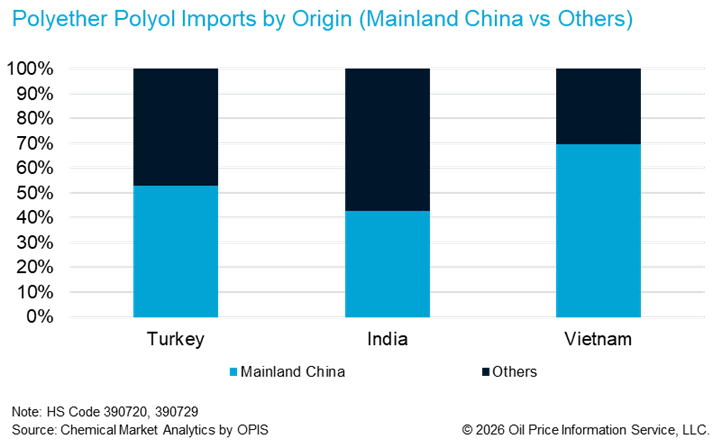

Mainland China accounted for 53% of Turkey’s total imports, while India imported 257 kt in 2025, representing 43% of its total intake. Vietnam had the highest concentration, with mainland Chinese polyether polyols accounting for approximately 70% of its imports in 2025 (Chart 1.3).

Given its scale and cost competitiveness, mainland Chinese origin material has effectively served as the global polyether polyol price reference in recent years, although this positioning has also led to multiple anti-dumping investigations and the imposition of duties in several markets.

The cancellation of the VAT refund on polyols exports may structurally raise mainland China’s export floor price by increasing net production and selling costs. In the near term, buying interest has been front-loaded ahead of the April 2026 implementation, supporting shipment volumes. After this order takes effect, export prices are expected to rise to reflect the revised cost base.

Some believe the change will lead to higher export offers. While mainland China is expected to remain a dominant supplier, pricing should moderate, and producers in Southeast Asia, South Korea, and the Middle East could see their positioning improve as global polyether polyol price differentials narrow. However, it is unlikely that they will be able to expand their market share significantly as a result of this new policy due to their inherently higher cost base.

Margin and Industry Structure

The presence of competitive polyether polyols exports from mainland China has mainly reflected an oversupplied market in the value chain. In recent years, the excess capacity build-up in propylene oxide (PO) and polyether polyols has kept margins thin. There have been periods when polyether polyols prices fell below those of PO – the feedstock for polyether polyols – resulting in negative or near-zero margins.

With polyols export companies no longer able to claim a VAT refund, their ability to absorb losses through purely volume-driven trade is reduced. Additionally, it is expected to drive several structural shifts across the polyether polyols industry. As well as lifting the basic cost of exports, smaller and non-integrated producers, particularly those without stable feedstock access or scale advantages, are likely to face mounting margin pressure. This would accelerate industry consolidation. In contrast, larger players, or those with integrated systems, should benefit from margin stabilization, with the ability to absorb higher costs and a more resilient polyols export position under the new policy framework.

Can the impact to polyols export companies be mitigated?

Large producers are assessing the “Import and Export Handbook” (often referred as “Processing Trade Handbook”) model, which allows propylene oxide (PO) to be imported under bonded status, converted into polyether polyols, and re-exported without incurring VAT or import duties. In simple terms, it is an electronic ledger that allows companies to import raw materials duty-free (no tariffs or VAT are paid at the border). This process has been widely used during earlier periods when VAT refunds were limited or unavailable. Following the unexpected announcement of the cancellation of VAT refunds for polyols exports, several major producers have begun exploring imported PO as a potential workaround.

Market Advisory Service – Global Polyurethane Feedstocks

Stay ahead with reliable price forecasts, supply/demand data, and strategic industry analysis

However, the model is only viable if imported PO is priced at or below domestic PO levels.

In recent years, domestic PO prices in mainland China have fallen sharply amid persistent oversupply and import economics have not improved to the same extent. Export availability from overseas PO producers has tightened as margins deteriorated, with some facilities idled or permanently closed. As a result, supply outside mainland China remains balanced to tight, limiting regional producers’ willingness to offer POs at competitive levels for re-export processing.

Implementing such a “Handbook” trade also introduces additional logistics and compliance costs. Bonded PO must be segregated in dedicated storage infrastructure and managed under strict customs supervision, raising operational complexity and capital requirements.

Therefore, this model is not scalable across the industry. As such, this model may soften the impact for large players but cannot fully replace the VAT refund mechanism.

Conclusion

Based on current information, we anticipate that, in the most likely scenario, producers will pass through roughly 50–70% of the additional cost burden arising from the cancellation of VAT refunds to polyols export customers. Competitive pressures in key export destinations and the need to preserve market share may limit the extent of immediate price adjustments.

As a result, margins for polyols export companies, particularly non-integrated and smaller-scale producers, are likely to remain compressed in the near term, even as offer levels trend upward.

Over time, the market is expected to gradually re-anchor to a higher price baseline through 2026–2027 as buyers adjust to the new cost structure and supply rationalization progresses.

Although mainland China’s export competitiveness will moderate, its position as the central polyether polyol price reference for Asia will remain intact. The removal of VAT refunds reduces structural downward pressure on global prices.

Overall, polyether polyols prices are expected to trend structurally higher than pre-policy levels. The market is unlikely to sustain pricing below marginal production costs over the longer term, reinforcing a transition from volume-driven expansion.

For comments and feedback, please reach out to: seeyan.wong@chemicalmarketanalytics.com