Déjà Vu All Over Again: Venezuelan and Iranian Sanctions’ Implications for Energy Markets

A few weeks into the second Trump administration, a new round of sanctions targeting Iranian and Venezuelan energy exports was announced. This was unsurprising, as both countries were sanctioned during the first Trump administration; however, the most recent round is significant because global oil markets are very different now than they were during 2017–18. A global pandemic, the energy crisis in Europe, and additional non-OPEC supply, among several other developments, puts the newly announced sanctions in a wholly different orbit. This piece will flesh out the commercial, geopolitical, and pricing implications of such sanctions.

The USGC industry competes with China for heavy barrels, as these two countries have the largest deep conversion (coking) capacity in the world.

Commercial implications: The world is running out of heavy crude, and this is a problem

Venezuelan crude exports are almost entirely heavy in nature, whereas the quality of Iranian crude exports is estimated to be around 40% heavy, with the remainder medium and light grades. Besides the obvious implication of disrupting global crude balances in general, sanctions on either or both countries significantly tighten the global heavy crude balance, impacting economics for complex refineries globally.

Notably, the context for heavy barrels was already challenging: In the last few years, the world has been consistently running out of heavy crude. The US Gulf Coast (USGC) refining industry was originally built around domestic light- and medium-quality barrels, as well as around Latin American supply of heavy grades (less than 24o API). These refineries include significant coking capacity, i.e., the technology needed to upgrade low-cost heavy barrels to high-value refined products.

The USGC industry competes with China for heavy barrels, as these two countries have the largest deep conversion (coking) capacity in the world. Heavy crude residue is fed directly to coking units to then extract gasoil and other streams, which will be processed to significantly increase gasoline and diesel yields for these refineries. A deep conversion refinery processing around 30–50% of heavy crudes in their slate usually enjoys a refining margin that can be more than 80% higher than a “generic” refinery, i.e., one that is geared to processing medium or light barrels (which are more expensive than heavy crude barrels).

Historically, crude experts used to call the three competing countries that traditionally exported heavy crude to the US Gulf Coast during the last 40 years “crude heavyweights”— Saudi Arabia, Mexico, and Venezuela. But times have changed.

Mexican and Venezuelan crude production and exports have declined significantly in the last few years. Saudi Arabia has adjusted its upstream production to maximize light- and medium-barrel exports and has increased processing in its refining system, thus reducing heavy barrel availability for the rest of the world.

Mexico was the most important heavy crude exporter to the United States for many years, but natural declines and pollution problems at its main fields (Cantarell) have reduced exports.

In fact, Mexico has announced plans to soon completely stop crude exports as its new Dos Bocas refinery goes into full operation mode.

The obvious substitute for sour grades in the United States is to bring Canadian crude all the way down to the US Gulf Coast. These barrels, however, are not nearly as heavy as the production and exports lost from the traditional heavyweights. On top of this, Canadian pipelines connecting to the United States do not necessarily serve all refineries in the eastern part of south Texas, Louisiana, Mississippi, and Alabama.

When considering all the technical details of this option, Canada is a palliative but not an actual substitute for heavy barrels globally. With the recently completed Trans Mountain Pipeline expansion, more Canadian barrels can penetrate the global (Asian) markets, which limits the net optionality for US Gulf Coast refiners to get those barrels.

Heavy grades are a scarce commodity. Additional heavy barrel sources throughout the world, such as Colombia’s Castilla, Ecuador’s Napo, or Argentina’s Escalante, are not able to ramp up supply due to lack of investment or geological declines. In the United States, the most important heavy barrel source was California’s domestic production (i.e., Kern River), which has also waned over the last few years. The only silver lining in the heavy crude world has been the Brazilian upstream sector, thanks to investments in the Campos and Santos basins, although not all this crude is heavy in nature.

Chinese refiners have traditionally balanced their crude slate with both Venezuelan and Iranian heavy barrels. Geopolitical and commercial factors have pushed these grades to Asia over the last 15 years, arriving to other countries like India or Indonesia as well, but China has been by far the most important market in the region.

As the Trump administration enforces a reloaded version of these sanctions, the reduction of both Iranian and Venezuelan crude exports has already impacted global markets. There is no easy solution to this rebalancing, so deep conversion refineries compensate for the lack of heavy barrels by processing medium-quality grades. US refiners have been ramping up runs of Canadian crude over the last few years, but the density differences mean that they need to process “more” barrels to obtain the same amount of residue to feed their coking units.

All in all, refining operations and margins are negatively impacted, thus reducing the competitive advantage of deep conversion refineries around the world. This reduces refined product supply and underpins price strength for products such as gasoline or diesel, which have not reduced their prices proportionally to the crude price reduction we have witnessed since January.

Even in Europe, where what remains of the industry is struggling to survive, regulators have faced severe resistance to how the energy transition is being handled: There have been calls for the de-bureaucratization of funding application processes and loosening of previously established decarbonization targets.

Geopolitical implications: The endgame

When exploring the geopolitical world, one can get lost in shallow details and rhetoric, so it is always paramount to identify what the endgame is for the counterparts involved: What seems to be the Trump administration’s final goal with respect to these two countries?

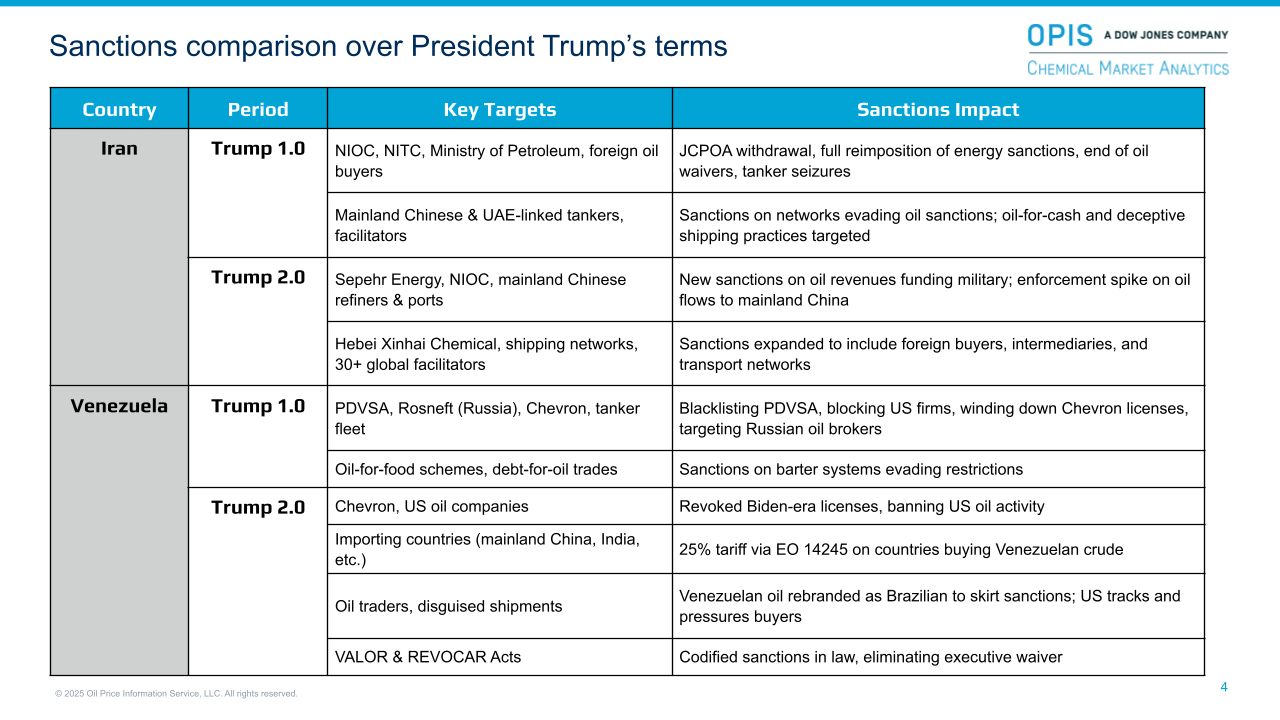

The decision to impose a new round of sanctions on Iran is inextricably linked to the close relationship between the US president and the Israeli prime minister. President Trump has met with Prime Minister Netanyahu over the years and has expressed full support for Israel in ending the Gaza conflict, with inherent combativeness towards Iran. Parallel to this round of sanctions—dubbed “maximum pressure”—negotiations over Iran’s nuclear program are underway.

Debilitating Iran’s financial resources and thus forcing the Islamic republic to be open to negotiations is paramount for the United States. A potential deal where Iran reduces uranium enrichment and is deemed a lesser threat to Israel might be on President Trump’s list of ultimate goals.

The US approach to Venezuela has been somewhat more benevolent than to Iran, though it can arguably be deemed more complex. Several US companies have operated in Venezuela over the years, creating issues related to expropriations and debt defaults, which has plagued Venezuela’s relationship with the United States in the past.

The US approach to Venezuela, including the most recent sanctions, is meant as a defense of democracy in the Western Hemisphere, ultimately allowing the rule of law to prevail, which is always an important requirement for international companies’ investments in any country.

In this context, the outcome related to the public bids for Citgo assets that are being held to pay several companies remains to be resolved by the US legal system.

The Trump administration does not see Venezuela as a national security threat. From the perspective of the energy sector, however, the United States might seek additional commercial concessions and guarantees of stability for foreign investment should American companies’ potential return to Venezuela be a desirable outcome for President Trump.

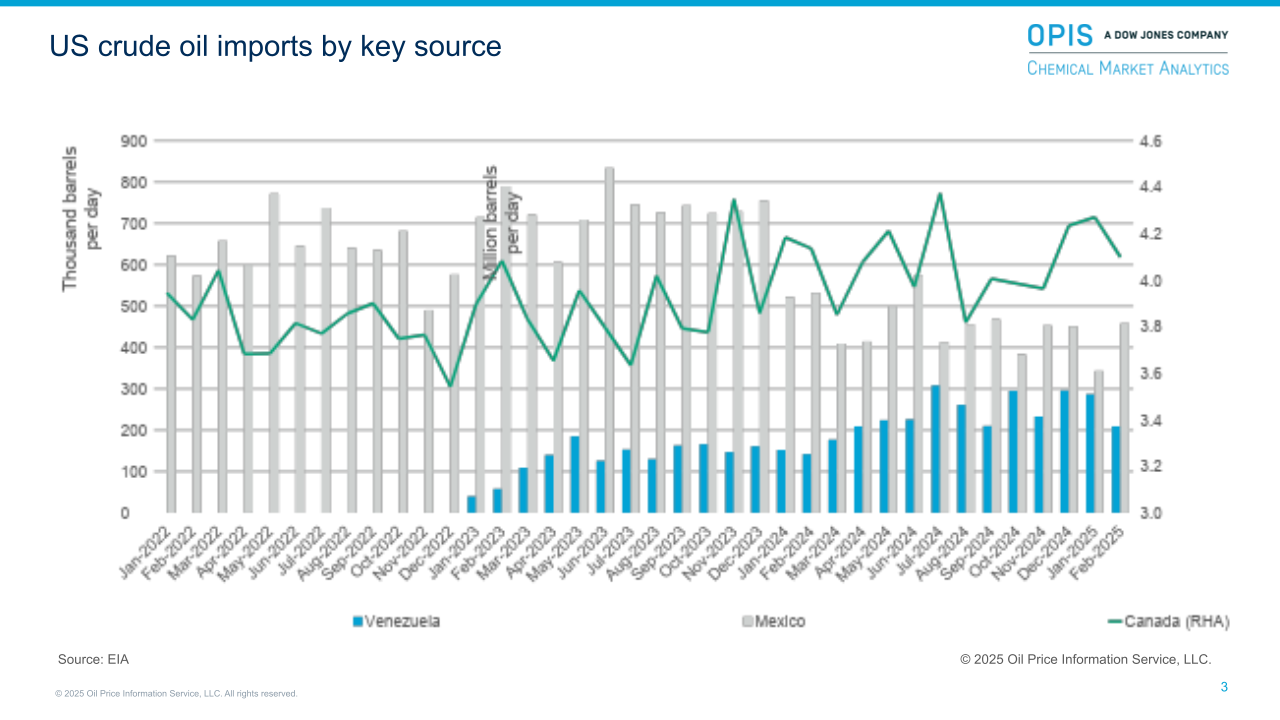

These sanctions arrive at the worst possible moment for Venezuela: Thanks to technical operations and investment from Chevron in the last few months, the country was able to ramp up exports, starting the year at almost one million barrels per day, with around 300,000 of those barrels going to the United States every day.

Although the sanctions on both countries are not new, the latest iteration has a new layer of sophistication. The United States has also announced sanctions on buyers of either Iranian or Venezuelan crude, meant to smother both sides of the commercial relationship.

Pricing implications: Heavy crude balance tightened, impacting price differentials

Commercial sanctions that interrupt crude trade from Iran and Venezuela create significant economic challenges for refiners, especially for complex refineries with coking capacity:

- The price of heavy grades increases, as the lower supply makes every available barrel more attractive to refiners.

- As complex refiners need to pay more for heavy grades or are forced to substitute with medium barrels, they could adjust operation rates or be forced to adjust their crude intake to compensate for their production targets, which reduces the amount of fuel produced. At minimum, refinery economics are severely impacted.

- The recent round of sanctions on Iranian crude has not only negatively affected Iran’s crude exports but also its core customer base—mainland China’s independent “teapot” refiners. Iranian crude arrivals at mainland Chinese ports have substantially declined in recent months, forcing these refiners to seek alternatives, including Russian, Latin American, and Middle Eastern barrels, or even fuel oil as substitutes.

- The resulting rise in feed costs is likely to further strain refining margins, compounding existing pressures stemming from subdued domestic fuel demand and Beijing’s ongoing drive to decarbonize. This current squeeze could accelerate a broader structural shift to phase out inefficient, small-scale operations in favor of more competitive greenfield refinery projects.

The complication around heavy crude markets goes far beyond a supply-and-demand reaction. The niche nature of this crude, with few producers in the world and specific refineries seeking it, means that most volume sold globally is done via long-term contracts. This heavy crude balance tightness impacts commercial teams as well as refinery operations in general.

- From an operational perspective, a refiner cannot easily shift from one type of heavy barrel to another, as it aims to optimize the handling of difficult properties, such as corrosion, metal content, and sulfur, among others.

- Therefore, a deep conversion refiner will always try to keep its crude slate as fixed as possible; its counterparts—crude exporters—will aim for a fixed roster of clients to supply. Virtually all heavy barrels in the world are sold under long-term contracts.

Beyond commercial relations, these sanctions affected price differentials as well. As already evident during the last few months, steeper sanctions on Iranian and Venezuelan grades primarily affected the Asian crude balance. This caused an uptick in the Dubai spot price, Asia’s unofficial market reference, during the first few months of 2025. The Dubai price strengthened, widening the arbitrage for crude shipments in Asia and other regions (Africa and Europe), which meant that Asia’s price strength attracted barrels from other regions to compensate for the gap left by Iranian and Venezuelan barrels, also underpinning price strength in the Atlantic Basin.

Sanctions directionally made crude and refined products more expensive globally. However, with additional OPEC+ supply and prospects of an economic downturn, the overall balance and price jitters have waned.

OPEC+ has responded over the last two months, announcing production increases that ended up being higher than originally anticipated. There is no doubt that the extended cartel has the volumetric capability to compensate for any additional supply impact. So, while crude supply is not currently a problem, overall differences in quality are likely to continue disrupting global markets for the months to come, with general tightness for heavy barrels.

The market will eventually exhaust its supply of economical NGLs (ethane, propane), as well as upstream light naphtha. Eventually, refineries will have to exponentially increase naphtha output, culminating in crude-to-chemicals complexes. This means that as oil versus chemicals demand forecasts stand, crude oil refinery assets must become directly positioned to make petrochemical feedstocks. The obvious essential motivator? Economics.

Conclusion: The winners and losers

Heavy crude producers like Argentina, Brazil, Colombia, and Ecuador will benefit from the sanctions as their crude prices strengthen in this environment. Canadian barrels will also gain, as they are the only realistic option for compensating heavy barrels in the United States and balancing the crude intake, which includes light crudes produced by fracking.

Conversely, refiners and integrated companies that own refining assets, mainly those with deep conversion capabilities that would typically translate to more competitive economics compared with other refiners, will likely have losses in the current sanction landscape.

Before President Trump’s latest sanctions on Iran and Venezuela, the world was already short of heavy crude, which has negatively impacted global refinery economics and prices. This new round exacerbates the problem, as it targets sources for a particular type of niche barrel that is not easily substituted by other global suppliers.

Complex, sophisticated refiners with the configuration to process heavy barrels are resorting to processing Canadian barrels or other crudes that are closer to a medium quality, forcing them to run at lower utilization rates, which means suboptimal levels and less product supply.