Soda Ash: Finding the New Baseline

The global soda ash market has been going through a structural reset. Shifting trade flows, heavier influence from policy in the form of tariffs and trade measures and expanding production capacity are redefining how the market operates, while consumption patterns are changing with new demand growth from solar and energy storage applications.

The soda ash market can be defined as oversupplied in 2025. After growing by 8.5% year-on-year in 2024, mainly in mainland China, world soda ash demand grew by 1.4% in 2025.

The soda ash market can be defined as oversupplied in 2025. After growing by 8.5% year-on-year in 2024, mainly in mainland China, world soda ash demand grew by 1.4% in 2025. The slowdown in demand coupled with a sharp increase in supply has changed the market from being relatively balanced in 2024 to an oversupply situation since the start of 2025.

In 2026, glass production is projected to account for 56% of global soda ash consumption. Flat glass continues to lead demand, followed by container glass. Between 2026-2030, solar glass is expected to the fastest-growing glass segment. During the same period, lithium carbonate share in the world is expected to be the fastest growing end use for soda ash.

The global geopolitical environment has remained highly volatile, particularly over the past few months. The US/Israel-Iran conflict has started to weigh on the global economy, contributing to a downward revision in world GDP growth, which is currently projected at 2.4% for 2026. Additionally, rising transport costs, combined with broader supply disruptions, have pushed up energy and raw material prices, increasing soda ash production costs across most regions globally, including India.

The Middle East and the Impact of War in Iran

The Arabian Gulf accounts for approximately 2% of global soda ash demand. Outside of Iran, the only soda ash production capacity in the Arabian Gulf is located in Saudi Arabia.

Iran’s capacity exceeds domestic demand, enabling the country to act as a net exporter. However, little to no soda ash has reportedly been exported from Iran since the end of February.

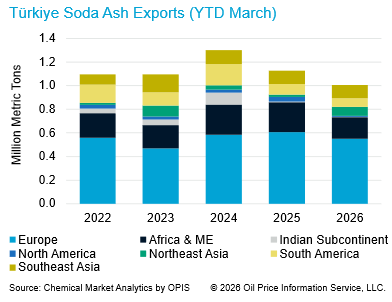

In 2025, nearly one quarter of Turkish soda ash exports were shipped to markets east of Türkiye, meaning a significant portion of this trade relied on the Suez Canal route. The Suez Canal and Red Sea trade routes are currently experiencing severe disruption. Nevertheless, the global market is expected to remain adequately supplied even if some trade routes continue to face interruptions.

Mainland China

Mainland China continues to dominate the global soda ash narrative. In 2023 and 2024, the country saw double-digit demand growth, primarily driven by solar glass production. However, this momentum hasn’t persisted into 2025. While both flat glass and solar glass production declined compared to the previous year, stronger lithium carbonate production helped offset weaker glass-related demand.

During the first quarter of 2026, domestic soda ash demand increased by 2.2%. Demand across downstream sectors, including glass and lithium-ion batteries, was supported by a temporary surge in activity as manufacturers accelerated exports ahead of the VAT rebate reductions implemented on April 1. Following this front-loaded demand, export activity is expected to ease in Q2.

Although natural soda ash capacity in mainland China has continued to expand, several Hou-process soda ash plants have remained idle since last year. These outages have officially been attributed to extended maintenance programs or technology upgrade projects. Taking both new capacity additions and closures into account, there is expected to be a net increase in effective soda ash capacity in mainland China in 2026.

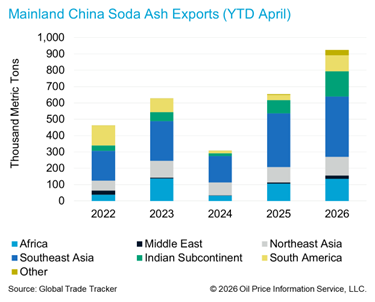

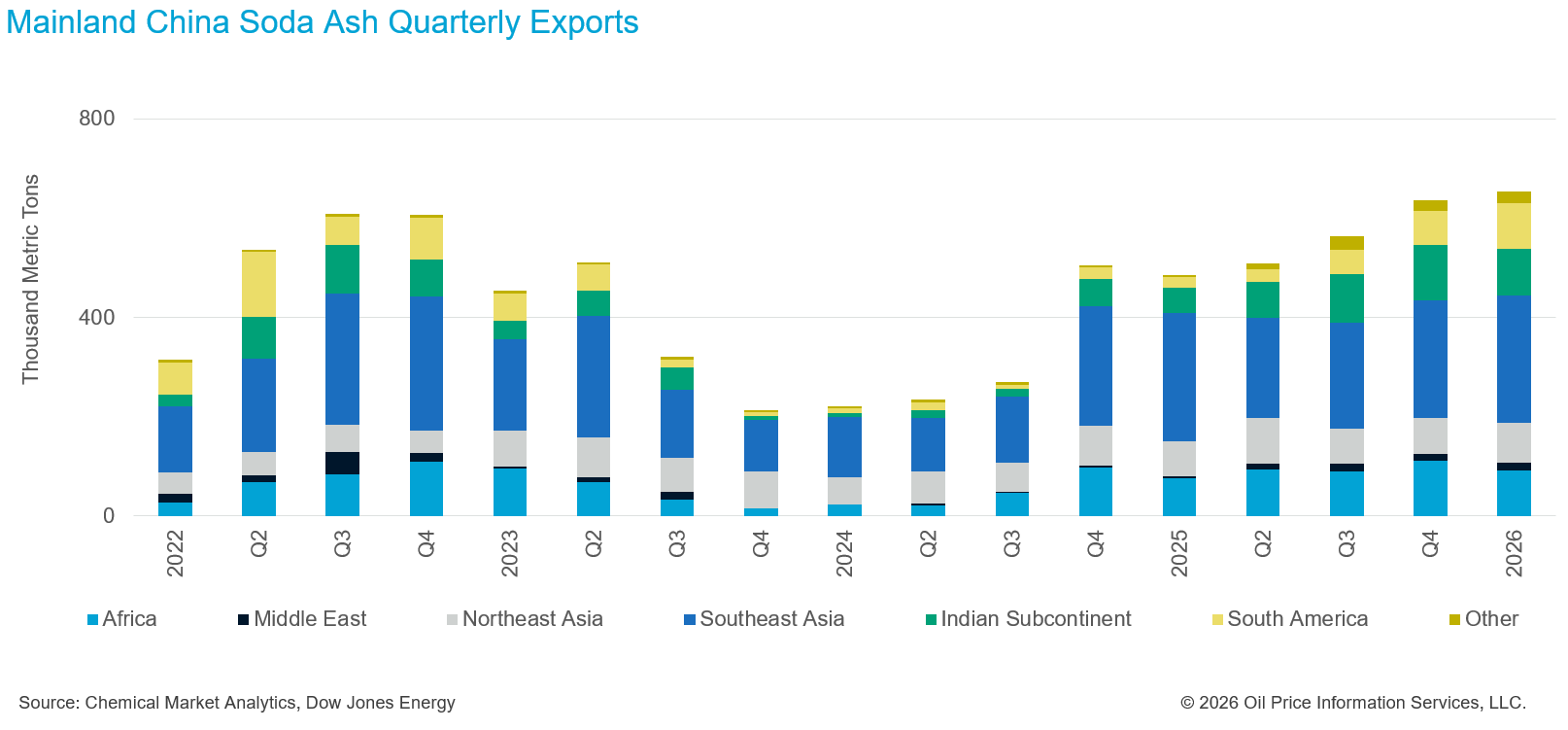

In April, mainland China’s soda ash exports rose by 41%, year-on-year totaling 925,000 mt. Higher bunker fuel costs following the onset of the Iran conflict improved the competitiveness of Chinese soda ash in nearby export markets. China’s surplus volumes are also increasingly reaching regions such as South America, which historically had not been a regular destination for Chinese product.

We expect mainland China to maintain an aggressive export strategy through the remainder of 2026 and beyond, in an effort to ease oversupply pressures in the domestic market.

Construction and Automotive Sectors are Expected to Support a Recovery in Flat Glass Demand

Flat glass is the largest end-use sector for soda ash. Global flat glass production is estimated to have declined by 1% in 2025, with only a modest recovery of less than 1% growth forecast for 2026. Medium- to long-term demand growth is expected to be driven mainly by developing regions and supported by both construction and automotive applications.

In 2026, EVs and hybrids combined are projected to surpass internal combustion engine vehicles in global production share for the first time.

Global light vehicle production increased by 3% in 2025 to 92 million units, while EV production grew by 21%, accounting for 28% of total output. Rising fuel prices and energy security concerns linked to the Iran conflict are expected to further accelerate EV adoption. In 2026, EVs and hybrids combined are projected to surpass internal combustion engine vehicles in global production share for the first time.

Growth in automotive production is supportive of flat glass and in turn soda ash demand, while increasing EV and hybrid output also boosts lithium demand, providing an additional source of soda ash consumption.

Container Glass Remains Under Pressure

Container glass represents the second-largest end-use sector for soda ash, supported by its longstanding role within the food and beverage industries.

However, the sector has experienced considerable challenges in recent years, leading to a significant number of plant closures across both the US and Europe. Between 2023 and 2025, nearly 3 million mt of container glass capacity was shut down, with a further 1 million mt expected to close by the end of 2026.

This decline has been driven largely by ongoing pressure on consumer spending, alongside a structural shift in consumer preferences toward low- and no-alcohol beverages. Despite these difficulties, there are early indications of a modest recovery in container glass demand. Although production declined slightly in 2025, wine-related volumes remained relatively resilient. For 2026, global container glass production is forecast to increase by 1% year-on-year. While this projected growth suggests the beginning of a recovery, the industry is expected to remain under pressure in the near term.

Photovoltaic Solar Panels Saw Extraordinary Growth in 2025

Solar glass is the largest growth driver for global soda ash demand. While PV installations maintained strong growth in 2025, this did not fully translate into higher soda ash demand due to significant overcapacity in mainland China’s PV and solar glass sectors. Despite rising domestic PV installations, Chinese solar glass production declined as demand was largely met through existing inventories.

This trend is expected to continue in 2026, with Chinese solar glass production is forecast to fall again, despite further PV installation growth. Given mainland China’s dominant position in global solar glass production, this slowdown is expected to weigh on global output.

Outside mainland China, however, solar glass production remained strong, with double-digit growth in 2025, and further double-digit growth forecast for 2026.

Lithium Carbonate is Continuing to Drive Soda Ash Demand

Soda ash demand for processing lithium is growing strongly, although it still accounts for a very slow share of total global demand. Double-digit growth was recorded in 2025 and is expected to continue in 2026, with most of the increase concentrated in mainland China.

Lithium demand growth is being driven by expanding EV production and rapid growth in utility-scale Battery Energy Storage Systems (BESS), the fastest-growing battery segment. Demand for lithium carbonate, mainly used in LFP batteries, is also growing faster than demand for lithium hydroxide used in high-nickel chemistries.

Mainland China remains dominant in global lithium refining, although its market share is expected to gradually decline. The phased removal of China’s VAT export rebate on battery products is also expected to encourage battery manufacturing expansion outside mainland China.

Trade is Growing Faster than Demand (Outside Mainland China)

Global trade plays a critical role in the soda ash industry, as many major demand centres do not have sufficient domestic production capacity. As a result, approximately 25% of global soda ash output is traded internationally.

In 2025, the US retained its position as the world’s largest soda ash exporter, accounting for nearly 40% of global trade volumes. Although US exports declined slightly to 6.7 million mt last year, exports are expected to trend upward over the coming years as additional production capacity is commissioned to serve growing global demand. US supply is primarily directed toward Southeast Asia — the world’s largest importing region — as well as Mexico, Canada, and South America, where US producers continue to benefit from a highly competitive cost position.

While Türkiye and mainland China remain key exporting countries, their longer-term export strategies are evolving. Türkiye’s export volumes are expected to gradually decline as a greater share of new production is absorbed by rising domestic demand.

At the same time, mainland China’s soda ash exports exceeded 2 million metric tons in 2025, with volumes projected to approach or surpass 3 million metric tons in the near future.

Soda Ash Supply

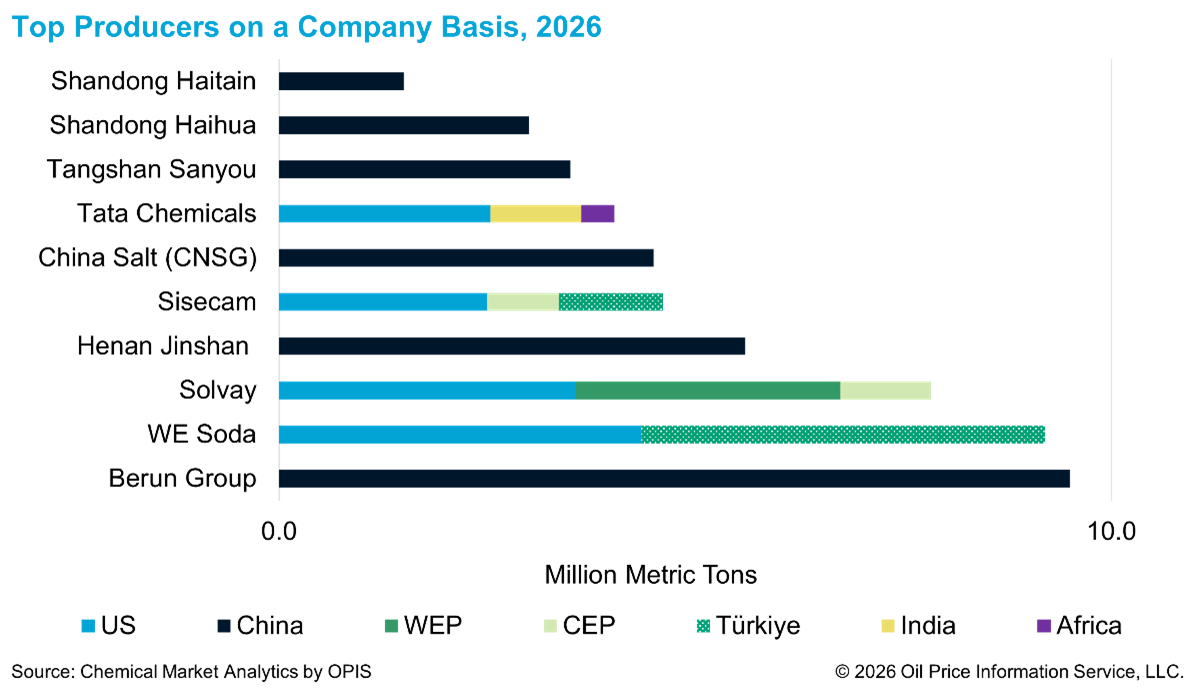

Mainland China has continued to dominate global capacity additions in recent years.

In 2025, the majority of new soda ash capacity additions took place in mainland China. By contrast, around 1 million metric tons of capacity was permanently closed in Europe during the year, driven by elevated energy costs, increasing EU regulatory pressures, and competitiveness challenges against lower-cost non-European producers.

Global net soda ash capacity is forecast to increase by close to 2 million metric tons in 2026. Growth will again be largely driven by major new projects in mainland China, more than offsetting permanent closures in the US and Spain, as well as temporary shutdowns currently affecting parts of the Chinese industry.

At the same time, there are new soda ash project announcements from countries that have not traditionally been producers, including Indonesia, Egypt, and Kazakhstan.

In the US, Searles Valley Minerals (SVM), owned by Indian conglomerate Nirma, mothballed its natural soda ash operation in California in February this year, marking the first US soda ash plant closure in more than two decades. SVM attributed the decision to high energy costs, California’s regulatory burden, and mounting competition from low-cost soda ash in seaborne export markets.

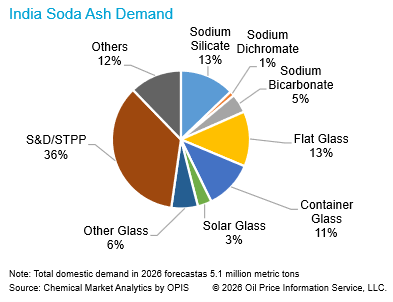

India

India is expected to grow faster than the global average in 2026, largely driven by new glass capacity additions, including solar, flat and container glass. A major driver is expected to be the solar sector. India is now the third-largest country globally in terms of installed solar power capacity and is expected to remain one of the main growth markets for solar PV.

This growth in soda ash demand for solar glass is further supported by trade protection measures. Anti-dumping duties on solar glass imports from China and Vietnam, along with countervailing duties on Malaysia, remain in place.

The war in Iran may none-the-less dampen the near-term demand outlook for India due to higher production costs and a potential for slower economic growth.

Also, in terms of local soda ash supply there are several cost pressures to consider. Higher than expected coal prices until early 2027 are likely to increase production cost.

In addition, limestone imports from the Middle East have been disrupted, which was accounting for more than 95% of total imports. Indian soda ash producers have increased the use of local limestone. Local limestone availability is sufficient, however is of lower quality, requiring higher usage rates. At the same time the price of locally sourced limestone has increased due to strong demand.

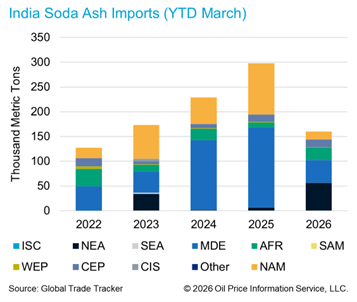

Bangladesh, which is entirely reliant on soda ash imports, has seen a significant shift in supply over the past year, with imports from mainland China increasing to around 55% in 2025, up from 19% in 2024. At the same time imports from traditional suppliers, India and Pakistan, have seen a reciprocal decline. The share of Indian soda ash in Bangladesh decreased from 42% in 2024 to 20% in full year 2025 and year-to-date March in 2026, losing its share to mainland China.

India which is a net importer of soda ash is expected to see a sharp decline in volumes from Iran this year; however, total imports are still projected to exceed 1 million metric tons in 2026, similar with last year, as lower supply from both Iran and Russia are expected to be offset by an increase in volume from mainland China. India’s exports to the Middle East accounts for about 10% of its total exports, equivalent to around 20 to 30 thousand metric tons per year which have been disrupted, but this loss in volume is not expected to significantly impact on the domestic market balance.

Costs and Margins

Soda ash cash costs are expected to increase across most regions in 2026 compared to last year, primarily driven by higher energy price outlook. Higher fuel costs drive an increase in raw material costs as well as leading to an increase in energy costs.

In contrast, the U.S. is expected to see a decline in cash costs compared to 2025, supported by a more favourable energy environment. Since March 2026, Wyoming natural gas and coal prices have remained mostly stable. The U.S. gas market has remained largely insulated from Middle Eastern supply disruptions, with Henry Hub front-month futures trending steadily downward.

This is creating a widening cost divergence across regions, particularly between US producers, European Solvay producers, and Chinese Hou producers, with the U.S. maintaining a relative cost advantage. However, U.S. producers are seeing an increase in their transportation costs, including domestic rail cost and in sea freight.

Outlook and Conclusion

One of the key factors shaping the soda ash market outlook today is slower GDP growth than anticipated at the start of the year.

At the same time, cost pressures have intensified. Coal and natural gas prices have risen across most regions since March, and higher oil prices have pushed up both land and sea freight costs.

On the supply side, there are no problems with availability. New capacity additions in 2026 are expected to more than offset the announced synthetic soda ash closures in mainland China. Similarly, recent closures in Europe and the US have had limited impact on the global supply/demand balance.

As a result, the soda ash market is likely to remain in surplus in the short to medium term.

That said, demand fundamentals are still supported by key growth sectors, particularly lithium and solar glass, which will remain key demand drivers. In fact, the conflict in Iran may act as a catalyst, potentially accelerating the transition toward new energy sectors as nations prioritize domestic energy security.

The upcoming World Soda Ash Conference in Valencia, Spain will be an important time to share views from key stakeholders regarding the industry’s strategic direction moving forward.