(Re)re-shaping the Energy Landscape: Structural Changes to Feedstock Markets

The energy market has faced significant disruptions in recent years, with political and societal factors significantly shaping the long-term market outlook.

This rapidly shifting landscape has fostered diverse views on the oil and gas markets: Some are convinced that the transition will be rapid, while others remain assured of hydrocarbons’ firm position as a key energy source. It is imperative that petrochemical market participants stay abreast of energy market shifts and the long-term feedstock implications. We are entering a transformational era for energy markets, which will culminate in structural supply changes for petrochemical feedstocks.

We are entering a transformational era for energy markets, which will culminate in structural supply changes for petrochemical feedstocks.

Chemical Market Analytics’ new Global Energy & Oil Demand Analysis weighs in on long-term projections for how energy markets will support forecasted petrochemical industry growth. Our base case scenario focuses on the long-term effects on feedstock availability in a world undergoing a structural shift in transportation fuel consumption and balances the external factors influencing the energy market outlook and the enduring impact on the availability and competitiveness of petrochemical feedstocks

Major political and societal factors affecting energy markets

The political environment is supportive of a renewed oil and gas investment wave and sustained demand growth

In his first days in office, President Trump prioritized fossil fuels over renewables, lifted electric vehicle (EV) adoption mandates, limited fund distribution from the Inflation Reduction Act (IRA), and withdrew the United States from the Paris Agreement.

The US government’s actions solidified a global trend already underway: a slowdown in the energy transition and decarbonization progress. The political pendulum is swinging to the right in many nations, generally hindering progress towards net zero.

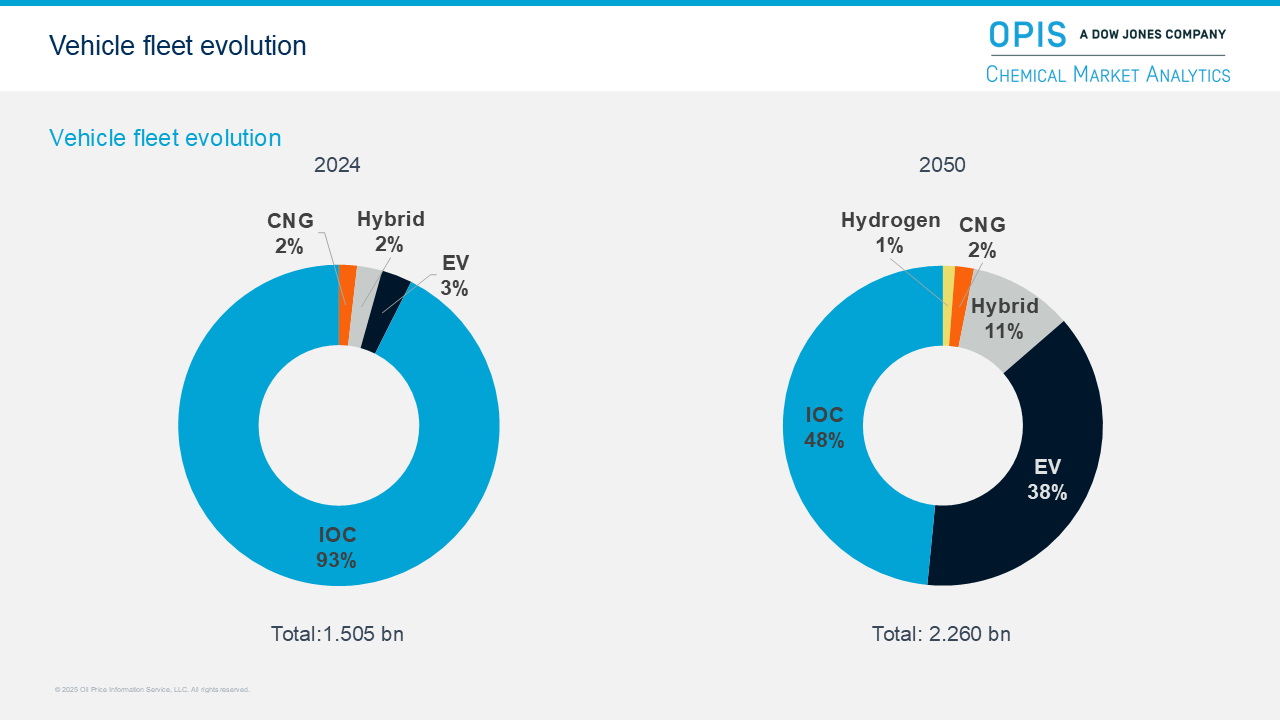

EV adoption rates take a step back, leading to a more gradual erosion of gasoline demand

Our base case scenario aligns with the OPIS view that developing regions’ fuel demand growth will offset demand declines arising from developed countries’ EV adoption (e.g. countries in Africa, South Asia, and Latin America). This is further supported by recent US policy shifts away from EVs in the short to medium term, and the clear slowdown in EV purchases in the European Union.

Chemical Market Analytics and OPIS forecast that the share of EVs in the overall fleet will gradually increase, but the number of vehicles that consume gasoline, like hybrids and conventional internal combustion engine (ICE) vehicles, will remain flat as hybrid vehicles gradually replace ICEs. This means that EV adoption will increase to accommodate the growth in mobility, not to erode existing mobility.

The rise of hybrids in the global fleet combined with vehicles’ growing gasoline consumption efficiency will still lead to a gradual decline in gasoline demand. The combined result of these factors is a more logical and measured evolution of gasoline demand rather than the EV-driven “shock” to gasoline markets often forecast.

Geopolitical tensions will redirect efforts away from net zero progress and toward energy security

The recently renewed—and escalating—trade war and ongoing geopolitical tensions have presented numerous crises that require imminent attention, currently diverting efforts away from regulatory progress supporting the energy transition. Energy security and affordability have increasingly taken center stage globally.

Even in Europe, where what remains of the industry is struggling to survive, regulators have faced severe resistance to how the energy transition is being handled: There have been calls for the de-bureaucratization of funding application processes and loosening of previously established decarbonization targets.

A very unlikely UN Plastics Pollution Treaty consensus supports growing virgin plastics production

Politics is also somewhat responsible for the lack of support for the UN Plastics Pollution Treaty, which may never come to fruition. This means that for the foreseeable future, there will be no global-scale coordination to reduce pollution and increase recycling, which would support higher virgin plastics (and fossil feedstocks) demand for longer.

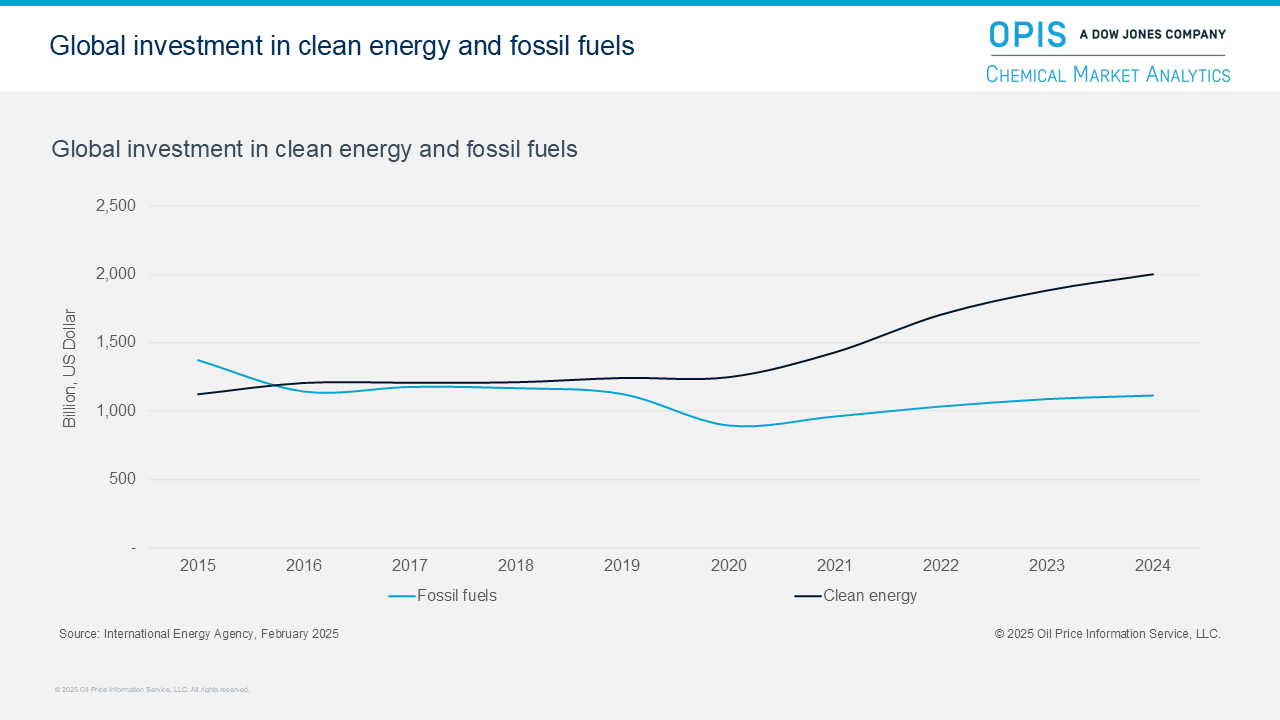

Profitability, interest rates, and the investment climate are unfavorable to renewables projects

Energy transition progress is decelerating due to political shifts but also due to many projects’ lack of profitability: Shell and BP have recently withdrawn from renewables projects due to poor economics.

While hydrocarbon-based energy is collectively accepted as a well-entrenched and still important source despite the energy shift, oil and gas majors are also widely expected to become “energy powerhouses” in a post–transition world, with businesses spanning fossils and renewables. However, there is a major challenge to doing so: Shareholder satisfaction. Pro-oil shareholders are leery of the losses accompanying renewables investments, while pro-renewables shareholders dislike oil’s ongoing prevalence in the industry. As oil majors diversify into renewables, the first steps will require delicacy in navigation: Most current shareholders are largely pro-oil, and they will assume more profitability if renewables projects are dropped.

The current investment climate is also unfavorable to Paris Agreement targets. Private-sector investment would have to ramp up significantly, but private finance groups have been stepping back from environmental, social, and governance (ESG) commitments (e.g., Blackrock’s latest exit from the voluntary Net Zero Asset Managers initiative, causing the latter to suspend activities). For existing renewables projects, high interest rates in recent years have contributed to poor performance, raising the pressure on returns and repayments. Additionally, more attractive investment returns in the AI sector have diverted funding from the energy transition agenda.

Powering AI demand requires fossil fuels, but will it be as big a boom as initially thought?

AI data center hubs require a steady source of power, and demand into this sector is projected to grow rapidly in the short to medium term. A holistic approach is needed: Wind, solar, and nuclear power; more grids; and, of course, natural gas and fossil fuel resources combined will be able to meet growing AI demand. That said, natural gas is a crucial, uninterrupted resource in the intermediate term.

Questions arose this year when DeepSeek significantly lowered long-term AI-driven power demand expectations. However, some analysts floated the Jevons paradox: More efficient, cheaper AI could mean faster, widespread adoption, thus an even higher and faster boost to energy demand than initially expected.

Our base case energy and feedstocks outlook

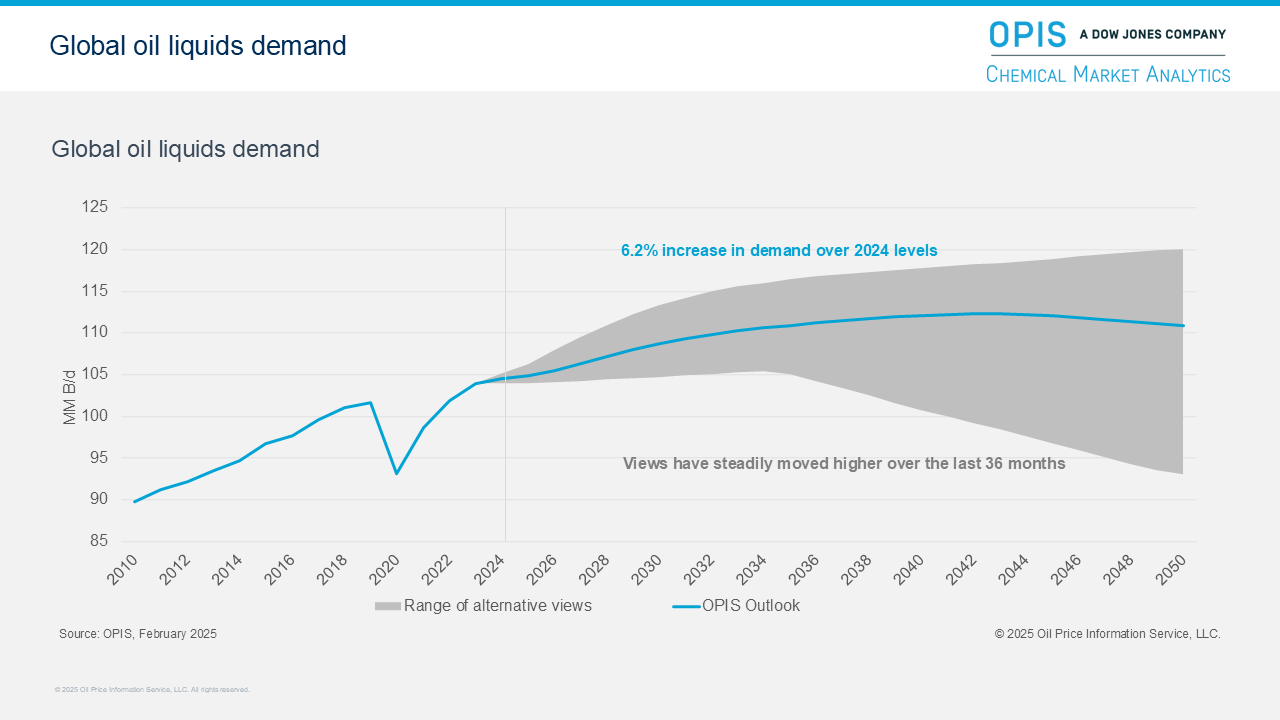

Base case global oil liquids outlook

The OPIS and Chemical Market Analytics outlook for oil demand includes two important drivers:

- 1. Fuel demand growth in developing countries will offset declines stemming from developed countries’ EV and hybrid vehicle adoption.

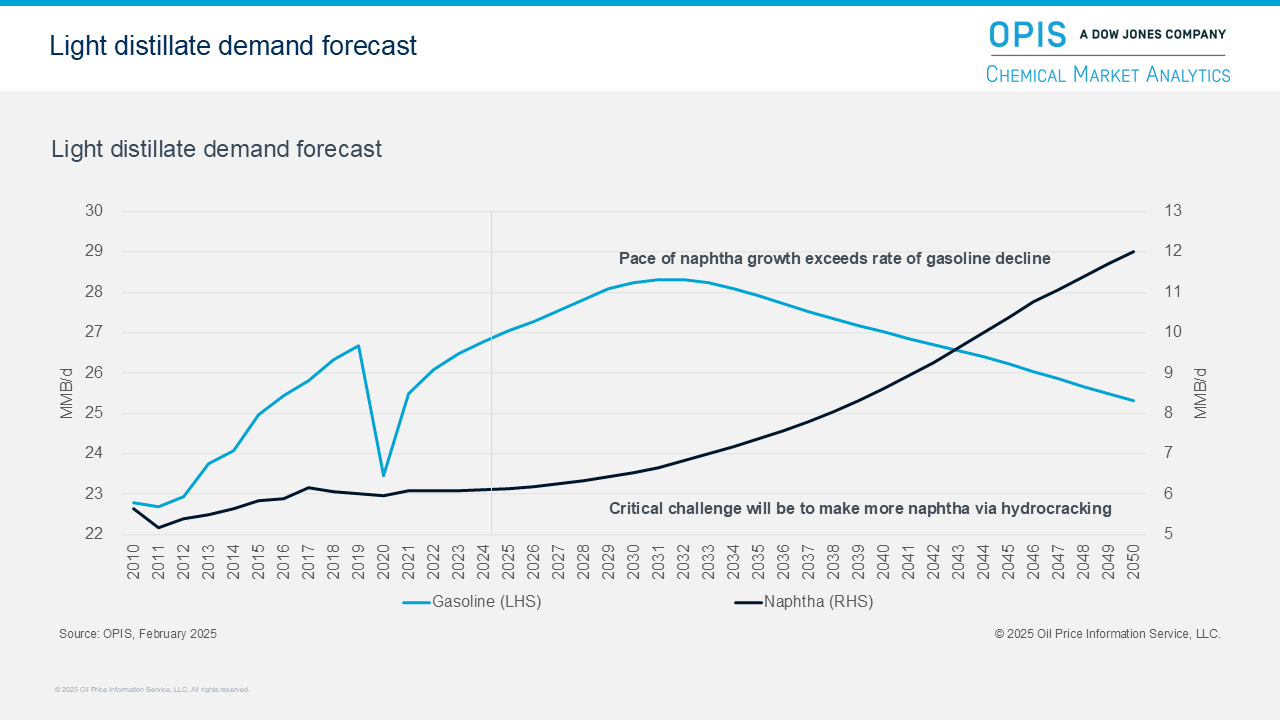

On the gasoline side, the changing vehicle fleet composition combined with continued growth elsewhere is expected to result in a 5.5% net decline in global gasoline consumption between 2024 and 2050. A moderate, pragmatic decline, but a decline nonetheless. This is important because in traditional refinery settings, less gasoline demand means less naphtha production, which is often the main feedstock for petrochemical value chains.

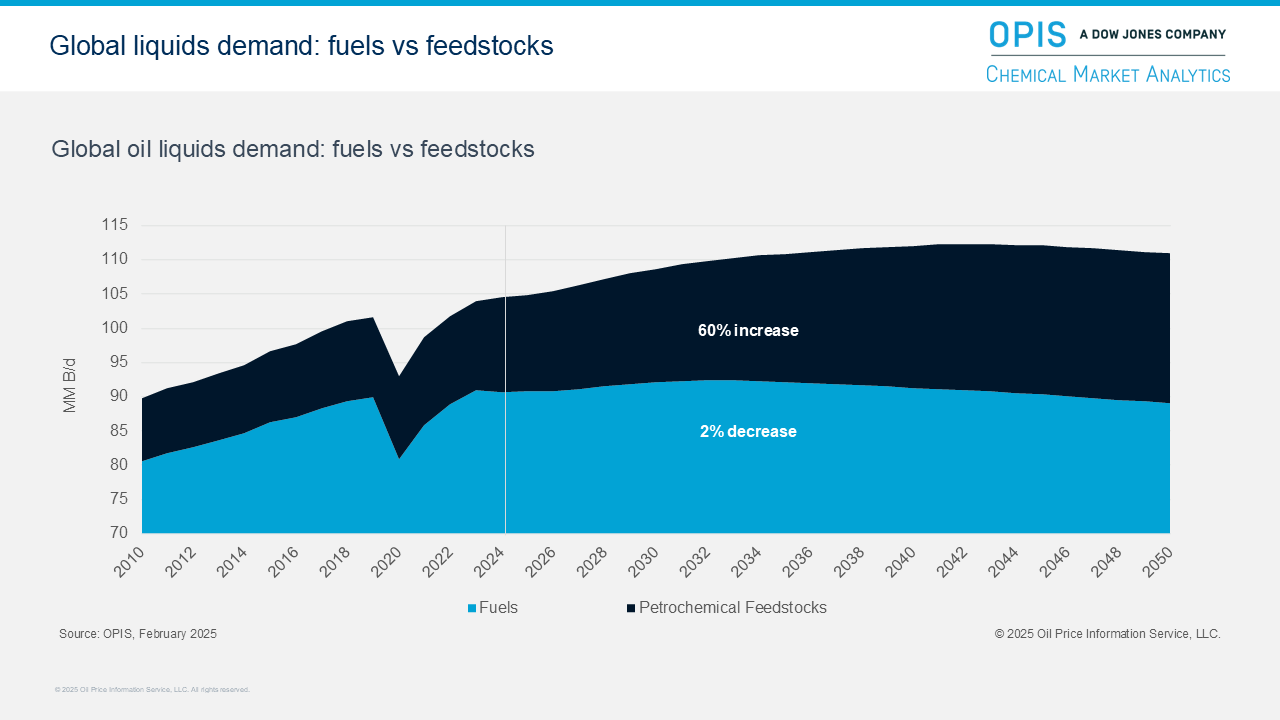

- 2. Petrochemical feedstocks will be the primary source of oil demand growth in the next 25 years.

In our base case scenario, oil demand will necessitate approximate current levels of supply throughout the forecast, mainly driven by petrochemical feedstocks (derived from robust plastics and synthetic materials demand). Oil liquids demand for petrochemical feedstocks will grow 60% by 2050, compared to only 2% fuel demand growth, meaning that on-purpose oil-based feeds will have to step in to fill the gap.

Petrochemical feedstock implications

The chemical industry has traditionally consumed unwanted hydrocarbon streams to create value products. Naphtha was only sold to chemical producers in absence of gasoline conversion or blending opportunities, ethane was separated from the gas stream to secure gas heat content specifications, and the chemical industry was the propane consumer of last resort. As we move forward, gasoline demand will plateau and then decline. Petrochemicals will become a core consumer of refinery output, creating major structural feedstock market changes in the long term.

Ethane

With the petrochemical sectors’ ongoing strong appetite for feedstocks, ethane consumption is poised for sustained growth. However, in the long run, each new ethane extraction will add another cost layer, and the finiteness of economically viable ethane will ultimately cap supply.

LPG

There is no peak in sight for LPG demand, with chemical-driven consumption expanding and leading overall growth. The battle between LPG for fuel use and petrochemical production will gradually intensify.

Naphtha

The fuel consumption decline will ripple across the refining and petrochemical industries, forcing refiners to recalibrate their production slates. Historically a by-product, on-purpose naphtha production will increase in a crude-to-chemicals approach to fill the gap and produce naphtha-equivalent barrels (e.g., via hydrocracking). However, a crack spread comparable to past fuel margins will be necessary to justify crude runs.

In short: If the industry needs more naphtha, it must pay more for it to incentivize refiners to run additional barrels to meet demand.

What is ahead for petrochemical producers?

The Chemical Market Analytics Global Energy & Oil Demand Analysis highlights a major gap between petrochemical feedstocks production and growing demand.

We have pulled all the potential refining levers to boost long-term petrochemical feedstocks supply without increasing total crude production in the long term. The resulting feedstock mix outlook reveals that petrochemical producers should brace for tight feedstock availability.

Navigating Tariffs, Transitions, and Tensions: From Mont Belvieu to Asia

10 September 2025, Raffles Hotel, Singapore

Register now →

Seats are complimentary!

The market will eventually exhaust its supply of economical NGLs (ethane, propane), as well as upstream light naphtha. Eventually, refineries will have to exponentially increase naphtha output, culminating in crude-to-chemicals complexes. This means that as oil versus chemicals demand forecasts stand, crude oil refinery assets must become directly positioned to make petrochemical feedstocks. The obvious essential motivator? Economics.