Clean Ammonia for Power Generation—Is the Hype Fizzling Out?

Most consumer goods and materials directly or indirectly contain ammonia. It is used in fertilizers, synthetic fibers, dyes, cleaning products, and many other applications. As we move towards global net zero, ammonia is gaining attention as both a major chemical industry greenhouse gas emitter and a prospective large-scale clean hydrogen carrier. Commercial ammonia production is transforming as a result: “Clean ammonia” can be mainly produced from fossil-based hydrogen combined with carbon capture, or from renewables-based hydrogen.

Among several emerging applications, clean ammonia has been considered to reduce coal-fired power plants’ CO2 emissions, especially in assets that are too young to retire. Such plants are prevalent in Asia, so most clean ammonia demand for power generation is forecast there also.

Japan and South Korea in particular have robust power sector decarbonization targets and are focusing on ammonia/hydrogen co-firing to achieve them. In the early-2020s, we saw a boost in research and development and signed memorandums of understanding linked to this type of ammonia use, but in 2025, the hype about ammonia for power generation seems to be fizzling out.

Japan and South Korea’s lead onset of clean ammonia into the power sector

The Japanese and South Korean governments were pioneers in incentivizing hydrogen and ammonia use to decarbonize hard-to-abate sectors, with power generation taking center stage amid targets and regulations. To increase domestic clean ammonia demand, the Japanese government targeted 3 million metric tons (mt) of use annually by 2030 and 30 million mt by 2050. This spawned multiple ammonia fuel production, transport, storage, and use projects, with many aiming to bring ammonia facilities online by 2030.

South Korea is also aiming to reach 20% co-firing in 24 coal-based plants by 2030 and raise the clean hydrogen or ammonia power generation target to reach 13.8–21.5% by 2050. Even if ammonia co-firing is only targeted at 20%, there is a huge potential for clean ammonia demand in the country.

“Clean ammonia” can be mainly produced from fossil-based hydrogen combined with carbon capture, or from renewables-based hydrogen.

Ammonia use for power extends beyond these countries: Many memorandums of understanding and ammonia combustion pilot testing projects are being conducted in cooperation with Japanese engineering and power companies elsewhere in Asia, namely India, Indonesia, Thailand, Vietnam, and Malaysia.

Given Japan’s and South Korea’s strong regulatory support and technological advancements for clean ammonia use in the power sector, it’s unsurprising that these countries are models for development in this sector.

Is technology ready to scale up?

Ammonia alone can be burned to generate power (direct ammonia combustion), or it can be part of a fuel mix (ammonia co-firing). Direct ammonia combustion has major downsides, especially its low combustion speed—it needs a much larger combustor than conventional fossil-based power plants—and the necessity of addressing nitrogen oxides (NOx) emissions.

Combustion speed can be easily addressed by adding other fuels to the mix, which also supports retrofitting ammonia co-firing feeds into existing power generation assets. Direct ammonia combustion technology is not quite there yet, but commercial scale 20% ammonia co-firing by heating value does seem achievable.

Most 20% ammonia co-firing pilot tests have reached comparable NOx emissions, lower sulfur oxides (SOx) emissions, negligible nitrous oxide (N2O) emissions, and operational performance rates similar to coal-only power generation. In 2018, IHI Corporation announced the first successful test at this co-firing rate. Several pilot-scale tests are underway across Asia, with many supported by IHI and NEDO (for example, Adani’s Mundra Thermal Power Plant Unit 1).

Last year, commercial-scale 20% co-firing was finally effectively tested: In March through June 2024, the Hekinan Thermal Power Station 1GW Unit 4 in Aichi, Japan, successfully ran commercial tests of 20% ammonia co-firing, using approximately 40 kmt of clean ammonia. The project was a collaboration between JERA, IHI Corporation, and NEDO. After the test, JERA announced it would start construction, including large-scale tank installation and storage, etc., in July 2024, with the aim of beginning 20% ammonia co-firing commercial operations at the Hekinan station in March 2025. JERA is planning to start commercial 50% ammonia co-firing demonstrations at Hekinan in 2028 and aiming for direct ammonia combustion by 2050.

Overall, technological readiness may currently be impeditive for higher co-firing rates, but 20% co-firing, which is specifically mentioned in South Korean 2030 targets, is ready to be deployed.

Why is offtake falling short of expectations?

Clean ammonia suppliers have voiced concerns to Chemical Market Analytics about demand. Some of these suppliers have offtake agreements with power companies in South Korea and Japan for this specific use—like JERA’s 500 kmt per year 2022 bid for 2027–40 supply—and volumes to these countries are falling short of initial expectations.

In 2020, Saudi Arabia supplied Japan with the first low-carbon ammonia shipment specifically for power generation; five years on, there has been limited progress in low-carbon ammonia trade for power generation.

Lack of government support is the main reason for slow development in the sector. Government market intervention is crucial for establishing a global clean hydrogen/ammonia market: Developing markets require high offtake to reduce production costs and, thus, prices. Co-firing clean ammonia into a coal-based power plant does not currently make for good economics.

An example of lackluster government support is the first auction under South Korea’s Clean Hydrogen Portfolio Standard (CHPS), which took place in December 2024. The CHPS was launched in May 2024, and it is the world’s first clean hydrogen power bidding market—a market to supply and purchase electricity produced from clean hydrogen. It uses a contracts-for-difference mechanism, which aims to bridge the gap between the wholesale power price and the levelized cost of electricity (LCOE) produced by hydrogen/ammonia. Under the CHPS, the South Korean government would purchase a fixed amount of electricity derived from hydrogen /ammonia each year. If successful, the share of hydrogen/ammonia-based electricity in the national grid would reach 2.1% by 2030 and 7.1% by 2036.

For 2024, the bidding volume was 6,500 GWh, with a contract period of 15 years and commercial operations needing to begin by 2028. However, in the first CHPS auction, only 11% of the total generation volume offered was subsidized. Notably, the price cap/ bid ceiling set by KPX, Korea’s electricity market operator, was deemed “unrealistic” by bidders; it was also not made public, making it difficult for bidders to ensure their applications met requirements.

The Japanese government also created a 15-year Contract for Difference scheme via the Hydrogen Society Promotion Act 2024 to bridge the cost gap and support the development of clean hydrogen/ammonia into power. The scheme assigns $19.2 billion through subsidies for low-carbon hydrogen and derivatives, locally produced and imported, and has been extended to include clean hydrogen/ammonia into other hard to abate sectors. Midstream developments and infrastructure, like ammonia terminals and storage tanks, are also supported.

In theory, the Japan Organization for Metals and Energy Security (JOGMEC) will subsidize the difference between the costs (strike price) and reference price calculation based on conventional fossil fuel alternatives. For hydrogen and low-carbon ammonia for power generation, this reference will be linked to traditional LNG and coal prices, respectively.

A Japanese supplier or importer, not the foreign exporter, can apply for the scheme by submitting a business plan to the Ministry of Economy, Trade and Industry (METI) in coordination with the hydrogen or ammonia end user. Market participants say the required 10-year post-subsidy commitment limits participation, as it adds up to a total business agreement of 25 years, at minimum.

The advent of clean ammonia power plants

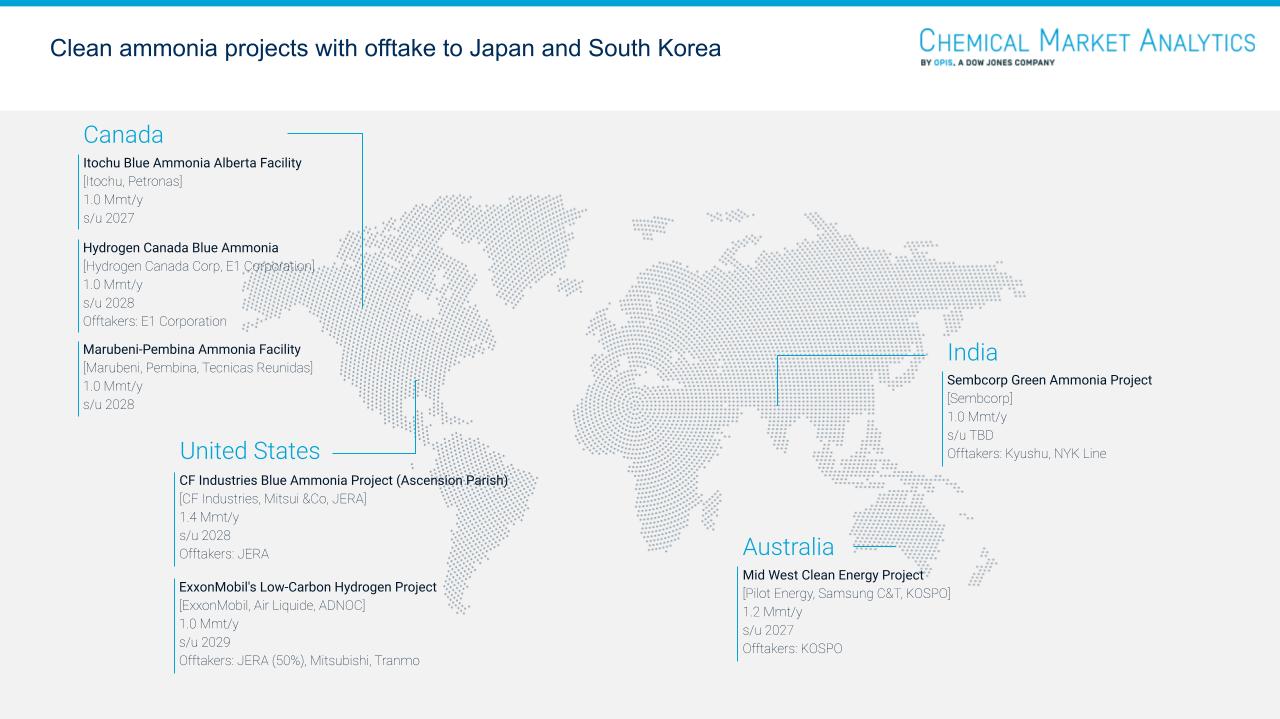

The single CHPS bid winner, KOSPO, is aiming to co-fire at least 20% of ammonia from July 2027 at the Samcheok Bitdream Headquarters power plant, Unit 1. Starting in 2028, KOSPO has committed to producing 750GWh of ammonia-coal co-fired electricity. The ammonia for this project will be CCS-based—produced with fossil fuels but using carbon capture and storage to reduce emissions—supplied by Australia-based Pilot Energy’s Mid-West Clean Energy Project, which aims to produce 1.2 million mt of clean ammonia annually.

KOSPO’s project comes with added infrastructure requirements. Samsung C&T will build the adjacent ammonia import terminal, including a 30 kmt storage tank and an unloading berth for up to 90,000 DWT ammonia carriers. The ammonia terminal and fuel supply infrastructure construction is slated for July 2027.

JERA’s ammonia co-firing plans at Hekinan in Japan and KOSPO’s Samcheok Bitdream project both seem well-advanced and likely to come to fruition, kicking off the global adoption of ammonia co-firing for power generation. It is still uncertain which other plants will make the ammonia co-firing transition before 2030.

Is there enough infrastructure to support demand growth?

Infrastructure spending is also a major hurdle to overcome in making the switch to ammonia co-firing. According to the Ammonia Energy Association’s ammonia storage terminal database, only about 0.5 million mt of announced ammonia storage capacity is expected to be built in Japan and South Korea combined; current operational storage capacity is 0.3 million mt.

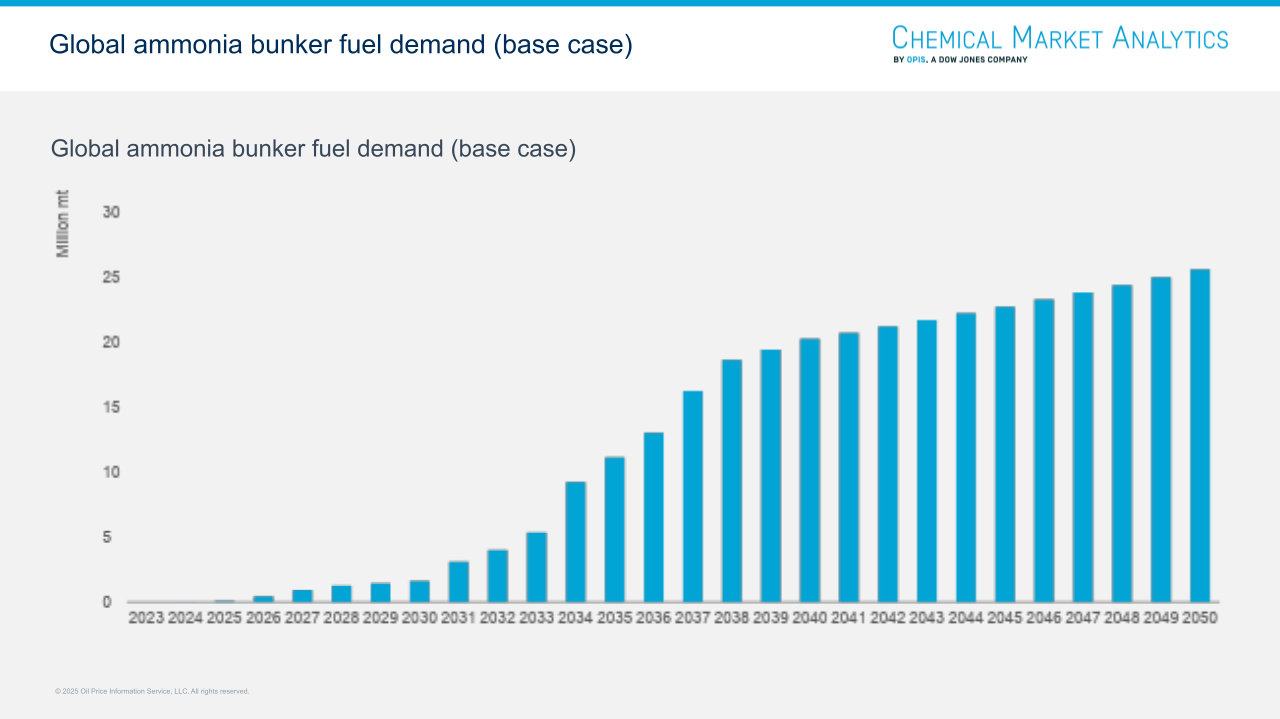

Chemical Market Analytics base case scenario puts clean ammonia demand for power generation in Japan and South Korea combined at 12 million mt by 2050, below the current government targets yet still necessitating significant infrastructure development.

Japan currently imports around 200-250 kmt of ammonia. Its ambitious ammonia co-firing use target of 20% by 2030 will require a substantial and sharp supply network buildup to accommodate more than 2 million mt of imports. Similarly, South Korea imports about 1.1–1.3 million mt today. Given its current coal-based power plant capacity of 3.5 GW and the hefty targets in place to decarbonize it, even if considering only 20% co-firing with ammonia, demand could reach 17 million mt per year.

Chemical Market Analytics base case scenario puts clean ammonia demand for power generation in Japan and South Korea combined at 12 million mt by 2050, below the current government targets yet still necessitating significant infrastructure development.

Building this much infrastructure is very costly. Using KOSPO’s project as a reference, the Samsung C&T contract to construct ammonia unloading, storage, and transportation facilities for the Samcheok, South Korea, plant cost KRW140 billion ($103 million).

A medium-term fix to a long-term problem makes for a poor business case

Perhaps ammonia use for power isn’t taking off because it seems transitory: Ammonia co-firing was initially intended as a fix to reduce emissions from coal-fired plants that were too young to retire. The challenges of direct ammonia combustion made it seem like an unlikely long-term solution. Some key market participants are making significant research and development progress into direct combustion by 2050, but to date, the economics are not feasible. Also, a coal plant running on 50% ammonia would still emit more CO2 than a gas-based power plant.

Another potential hindrance to longer-term investments in ammonia-fueled power plants is whether it makes more sense to run them on hydrogen rather than ammonia, as ammonia cracking is also being considered as a precursor to power generation.

This comes with significant efficiency losses as cracking technology stands today, but even Japanese government policies consider ammonia as “a fuel in transition period to hydrogen-powered society”, which could be perceived as hydrogen combustion being the ultimate goal for power generation.

As a result of all these factors, there are no known commercial-scale plans to build new solely ammonia-run power plants, and we project strong competition from other feedstocks for new power generation asset builds in the region.

Indeed, the business case for clean ammonia into power was mainly built on regulatory mandates and targets that were rather medium-term for the scale of a power plant lifecycle, which is typically up to 70 years. Without significant government support and stricter mandates, long-term clean ammonia demand for this sector is unlikely to take off.

Where else could clean ammonia demand pick up?

The tepid ammonia-to-power market take-off could also be indicative of a slower ramp up for other new clean ammonia end uses. The Japanese and South Korean technology developments and regulatory framework for clean ammonia use for power are fairly solid compared to other countries and other applications. If power generation demand in these countries is falling short of expectations, it raises questions for other clean ammonia uses, such as marine fuel, steel production, etc.

But other clean ammonia demand hubs are on the rise. Europe and Singapore are eager to build hydrogen hubs, especially in major bunkering terminals.

In Rotterdam, nine hydrogen/ammonia projects have been announced for the coming years, underpinning Rotterdam’s ambition to import 18 million mt per year of hydrogen equivalent by 2050, becoming Europe’s premier hydrogen hub. Ammonia imports will be key for this; however, limited projects have been confirmed at the final investment decision (FID) stage, mirroring wider sector development.

The Netherlands is aiming to phase out coal-fired power plants by 2030 and has hydrogen use in industry targets. Thus, clean-energy imports will be important. Rotterdam is also part of the MAGPIE project to supply and use green marine fuels to, from, and in various ports. The port’s particular focus is an ammonia bunkering demonstration in early 2025.

In July 2024, the Singapore Energy Market Authority (EMA) and the Maritime and Port Authority of Singapore (MPA) shortlisted two consortia for the next round of proposal evaluations for the Jurong Island power generation and bunkering ammonia hub. The consortia will conduct engineering, safety, and emergency response studies for the project.

There are still significant challenges to using ammonia as a marine fuel, so we project that ammonia will play a comparatively small part in the new maritime fuels picture, even by 2030 onward.

The next stage will select a lead developer for 55–65 MW of power generation via direct ammonia combustion in a combined cycle gas turbine using imported low- or zero-carbon ammonia and to build ammonia bunkering capacity of at least 0.1 million mt per year. The developer should be announced in the first quarter of 2025.

There are still significant challenges to using ammonia as a marine fuel, so we project that ammonia will play a comparatively small part in the new maritime fuels picture, even by 2030 onward. On the upside, the International Maritime Organization (IMO) is becoming more favorable to using ammonia as a bunkering fuel: As of 1 July 2026, ammonia can be used as a fuel on gas carriers, but the IMO guidelines are not mandatory, and they will be reviewed in 2026 or 2027.

While both Europe and Singapore seem set to build hydrogen/ammonia hubs related to power generation and bunkering, the nascent nature of most of these technologies makes the economics challenging. Rapidly evolving regulatory landscapes have the potential to easily reshape the clean ammonia industry and demand projections.

Global Ammonia Analysis by Chemical Market Analytics supports market participants with short-term and long-term forecasts spanning traditional and low-carbon markets, helping them navigate this fast-moving, transformational era for ammonia markets.